0% or 30% Tax on Foreign Dividends?

International Tax mechanisms and income strategies

Two things in life are inevitable: death and taxes. While the first is beyond our control, the second can be managed, especially when it comes to your international income investments. For global income investors, taxation is often the hidden drag on performance. What’s the point of diversifying across borders and targeting high-yielding dividend stocks if taxes quietly erode most of your returns?

To build an efficient global income strategy, you need to know exactly how your cross-border income — dividends, interest, and royalties — will be taxed. This understanding isn’t just a compliance issue; it’s a core component of portfolio construction. In this first part, we’ll look at how to calculate your effective foreign dividend tax rate — the real percentage you end up paying after both foreign withholding and domestic taxation. Knowing this figure is the foundation for optimizing your after-tax yield and choosing the right markets for income investing.

I/ How to Calculate Your Effective Foreign Dividend Tax Rate?

A/ Your Real Foreign Dividend Tax Rate Explained — in 3 theoretical Steps

As a global income investor, understanding your true tax burden on foreign dividends is crucial because a high gross yield means little if taxes eat most of it. The “effective” tax rate represents what you actually pay after factoring international withholding and domestic taxes. Here’s a straightforward way to calculate it:

Step 1: Identify the Foreign Withholding Tax

When a dividend is paid from a foreign company, the source country usually deducts a withholding tax before you receive it. This is your first tax layer.

Example: A French company paying a €100 dividend to a foreign investor may withhold 12.8%. Then, your broker credits 87.20 euros to your account.

Source: Pipart Global Income Investor Tools

Important: Tax treaties often reduce this rate, so always check the treaty rate, which is usually lower than the standard domestic rate. In that case, it depends on the country you live in.

Step 2: Calculate Your Domestic Tax Liability

After receiving the net dividend, your home country may tax this income differently depending on its system:

Credit System (common in US, UK and other European countries): You report the full gross dividend income but receive a credit for taxes paid abroad.

Exemption System: Some countries only tax the net income received after foreign withholding.

Step 3: Apply the Foreign Tax Credit to Determine the Effective Rate

To avoid double taxation, your domestic system grants credit for foreign taxes paid, provided a double taxation treaty (DTA) is in place. The effective tax you pay becomes the higher of the two rates, as the credit is limited to your domestic tax liability.

Scenario 1: Foreign withholding tax = 15%, Domestic tax = 15% → Full credit given, effective tax = 15%.

Scenario 2: Withholding tax = 10%, Domestic tax = 15% → Credit only for 10%, you pay extra 5%, effective tax = 15%.

Scenario 3: Withholding tax = 20%, Domestic tax = 15% → Credit capped at 15%, excess 5% unrecoverable, effective tax = 20%.

Practical Insight

Your effective tax rate depends on which tax (foreign or domestic) is higher. Investing in countries with withholding tax rates close to or below your home country’s rate maximizes net income. Always review tax treaties carefully and consider professional advice for complex international situations.

B/ In Practice: Favor Simplicity and Efficiency

Once you understand how foreign and domestic taxes interact, the next step is to apply these principles efficiently. In practice, the most successful global income investors are not necessarily those chasing the highest gross yields — but those who minimize friction costs, including taxes and bureaucratic complexity.

Prefer treaty-friendly jurisdictions

Countries with strong tax treaties (such as the US, UK, or Canada) typically reduce their standard withholding tax rates to 10-15% for treaty residents. This serves a dual purpose: it immediately lowers the tax burden at the source, and it simplifies the process of claiming foreign tax credits in your home country, as the credit you receive closely matches the tax you’ve actually paid.

While navigating treaty benefits may seem complex initially, the process becomes straightforward with practice. The underlying principles are standardized, often based on models like the OECD’s below (thankfully, you won’t need to read its articles in your daily investing).

Choose brokers that handle withholding at source

Some brokerage platforms automatically apply treaty rates at source, avoiding complex refund claims and administrative burdens.

Invest in zero withholding tax countries: simplicity as an advantage

Investing in countries with a 0% dividend withholding tax (e.g., United Arab Emirates, Singapore, Hong Kong) offers more than zero tax — it provides zero administrative hassle. With no tax withheld, you avoid lengthy, complicated reclaim procedures involving:

Extensive paperwork such as proof of residence and withholding certificates

Refund timelines that can stretch months or even years

Uncertain outcomes with possible partial or complete denial of refunds

This simplification reduces time, effort, and costs, allowing investors to focus on portfolio selection and growth rather than tax paperwork. Receiving gross dividends directly also improves liquidity and reinvestment speed.

Avoid countries with high unreclaimable taxes

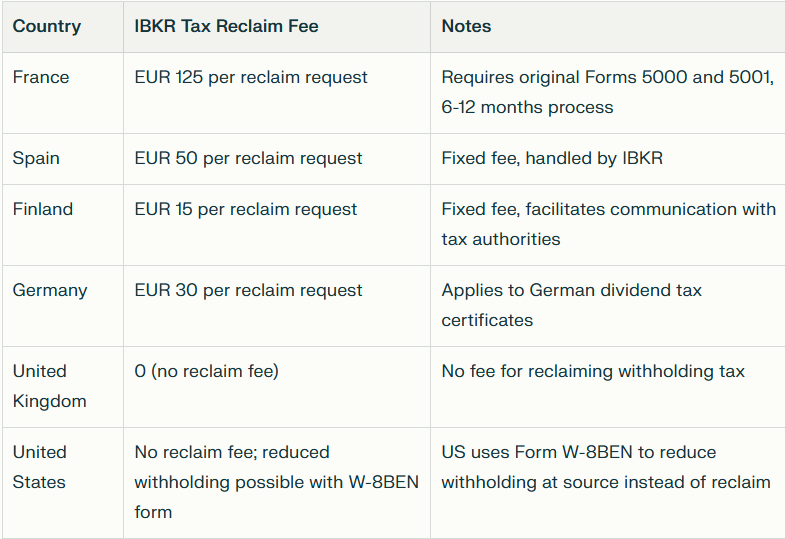

This creates a permanent and unavoidable drag on performance, making it nearly impossible to achieve a competitive net return. Markets with withholding rates exceeding 30%, often with no or limited reclaim options (like Switzerland and some Asian countries), introduce significant friction and reduce net income. Moreover, some reclaims are not cost-effective. For example, Interactive Brokers, a well-known global brokerage platform, may charge fees in certain cases for processing tax reclaims. See below:

By favoring jurisdictions and brokers that minimize tax friction, and by leveraging zero withholding tax countries when possible, investors can build a simpler, more efficient global income portfolio that maximizes after-tax returns with less administrative burden.

In conclusion, to maximize your net returns:

avoid jurisdictions with withholding tax rates higher than your domestic rate,

reduce administrative complexity by selecting a broker that handles tax documentation efficiently,

and prioritize investments in countries with 0% dividend withholding tax where possible.

II/ Advanced Tax Engineering: Optimizing Complex International Income

While Part I covered the fundamentals of calculating your effective tax rate, sophisticated income investors can further enhance returns by mastering specialized structures and instruments. This section explores advanced strategies for navigating hybrid securities, complex jurisdictions, and efficient portfolio construction.

A/ Case Study: Brazil’s Dual-Income Challenge

Brazil presents a fascinating case study in why understanding the legal nature of income matters. While the country imposes 0% withholding tax on standard dividends, it applies a 15% withholding tax to “Interest on Equity” (Juros sobre o Capital Próprio) payments.

Corporate Strategy vs. Investor Reality: Companies use Interest on Equity as a tax-deductible alternative to dividends, creating a corporate tax advantage. For international investors, this means the same company can distribute both tax-free dividends and taxable interest payments throughout the year.

Practical Impact: As Petrobras’ distribution history shows, an investor might receive a tax-free payment in one quarter, then see 15% withheld from the next. This variability makes accurate cash flow forecasting challenging and underscores why labeling Brazil simply as a “0% withholding” country is misleading.

Source: https://www.investidorpetrobras.com.br/en/shares-dividends-and-debts/dividends/

Investment Implication: Success in these markets requires moving beyond static withholding tax tables to active payment monitoring. Your broker’s dividend statements become essential forensic documents, requiring careful review of each payment’s classification.

B/ The US Landscape: Mastering REITs and MLPs

The United States, a core market for most investors, presents its own set of complexities with unique structures like Real Estate Investment Trusts (REITs) and Master Limited Partnerships (MLPs).

REITs (Real Estate Investment Trusts):

Their distributions are often classified as “Return of Capital” (ROC), ordinary dividends, and capital gains.

The Impact: A significant portion of the payment (ROC) is not immediately taxable. It reduces your cost basis, deferring taxes until you sell the asset. This is a powerful tax-deferral tool, but it complicates your annual tax filing (requiring a K-1 or Form 1099-DIV form in the US for some structures).

Withholding: For non-residents, the standard 30% withholding on dividends applies to the entire distribution, which may not be tax-efficient given its complex nature.

MLPs (Master Limited Partnerships):

These are even more complex for non-US investors. They generate pass-through income, and the tax liability is based on the fund’s business activities, not a simple dividend.

The Major Hurdle: They can create a US tax filing obligation (via a K-1 form) and may generate “Effectively Connected Income” (ECI), which is subject to higher, business-level taxation for non-residents.

The Investor’s Takeaway: While US REITs and MLPs can offer high yields, they introduce tax complexity for the international investor. Some REITs require careful tracking of cost basis, and MLPs are often best avoided due to the daunting US tax filing requirements. The administrative burden can sometimes outweigh the yield benefit.

C/ The “ETF Loophole”: Simplifying Access to Complex Markets

How can you access the high yields of a market like Brazil or the US real estate sector without the administrative headache? The answer for the strategic investor often lies in using Irish-domiciled ETFs as a tax-efficient wrapper.

The Mechanism: Instead of buying Petrobras shares directly, you invest in an ETF listed that holds Brazilian stocks.

The Tax Advantage of Irish ETFs:

Ireland has favorable tax treaties with both the US and Brazil, reducing withholding taxes at the source.

The ETF itself is taxed efficiently within Ireland.

You, as the investor, receive a single, simplified dividend from the ETF, which is typically subject to a straightforward 15% withholding tax (or 0% for EU residents in some cases), regardless of the underlying assets’ complexity.

The Investor’s Takeaway: For exposure to markets with complex local tax rules (Brazil) or for income from problematic structures (US REITs), holding them through an Irish-domiciled ETF can be a far more efficient and simpler option. It outsources the tax complexity to the fund structure, providing you with a clean, predictable income stream.

D/ The Execution Framework: Three Pillars of Tax-Efficient Investing

Translating this knowledge into a resilient portfolio requires a disciplined system built on three pillars:

1. Broker Selection as Foundation

Choose platforms that automatically apply treaty rates, provide detailed tax documentation, and flag potentially problematic investments before execution.

2. Operational Due Diligence

Implement systematic processes for:

WHT Verification: Confirming applied rates match treaty expectations

ADR Fee Monitoring: Tracking custody fees that silently erode yields

FX Impact Awareness: Understanding how payment date exchange rates affect net income

3. Strategic Jurisdiction & Instrument Selection

Build around inherently efficient options:

Prioritize 0% withholding and treaty-friendly jurisdictions

Utilize Irish ETFs for complex market exposure

Systematically avoid high-withholding, non-treaty countries

Advanced tax optimization isn’t about eliminating complexity but strategically managing it. By understanding specialized instruments, leveraging efficient structures like Irish ETFs, and implementing disciplined operational processes, investors can capture global yield opportunities while maintaining portfolio simplicity and regulatory compliance.

Investment takeaway

“Fiscal complexity,” identified as one of the main obstacles to international diversification, is perfectly manageable. With the information from the first part of this article, you can fully understand the issues before investing and read your broker’s dividend report.

All it takes is:

Avoiding the few mistakes identified in this article (excessively high WHT, overly complex reclaims, misunderstanding the fiscal nature of the income paid out)

Training yourself to understand the legal and fiscal issues. In my opinion, the information provided in this article is enough to see things clearly and start international investing—or monitor it—without anxiety.

So you can therefore calmly build your strategy using the tools (dividend withholding tax by country table) and the reasoning provided.

The few difficulties mentioned are largely outweighed by the pleasure and peace of mind offered by an international diversification of income. It provides indispensable security with a view to retirement, a gradual cessation of professional activity, or for joining the FIRE movement.

In short, with the right broker, basic tax literacy, and a disciplined approach to jurisdiction selection, international income investing becomes a source of stability — not complexity. This small, initial effort opens the door to global opportunities and long-term financial peace of mind.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

Disclaimer: This article is for informational and educational purposes only and should not be considered financial or investment advice. The views expressed are solely those of the author and do not constitute a recommendation to buy, sell, or hold any security. Always conduct your own research and consult with a professional before making any investment decisions.