12 % Yield, 14 % Total Return YTD – Early Lessons from Building a Global Income Portfolio

Good results in a bull market

Can a portfolio generating a high level of dividends avoid destroying its initial capital? This is the perennial question and the core issue that has tarnished the reputation of income investing, especially in an era dominated by growth strategies—a time when even dividend growth strategies can be mocked. But let’s be honest: many investors do not have a large enough portfolio to generate meaningful income from a dividend yield between 2% and 3%. Even with 200k USD invested, a 2% yield only gives 4kUSD per year—barely enough for a few utility bills

As for growth strategies, however high performing they may be, few investors are capable of managing their complexity during retirement. And, in any case, they sometimes discover that you can’t pay bills with paper gains. Let alone with paper losses. It is precisely to explore this alternative path that we are examining the year-to-date results of this model portfolio dedicated to income. Here is what we will cover: the breakdown of its performance, the sources of its income, and the critical risks that lie ahead.

I/ Balancing High Yield and Capital Appreciation: A Promising Start

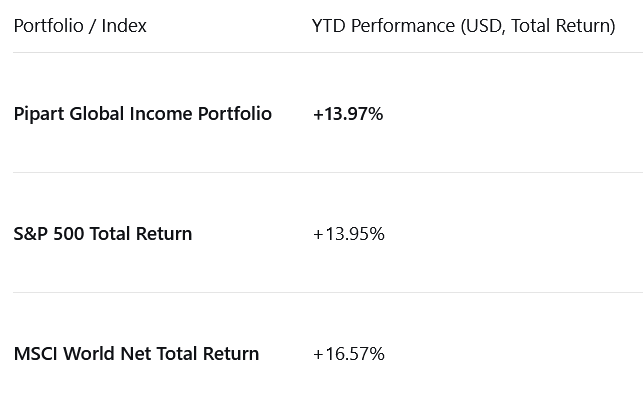

A/ 13.97 % total return YTD: not too bad for a high yield portfolio.

The most noteworthy aspect of these results is the combination of a high yield with solid capital appreciation. Typically, one might expect a portfolio focused on generating a 12% yield to see more muted capital growth. Therefore, it’s significant that the portfolio’s total return of +13.97% has closely matched the +13.95% return of the S&P 500 this year (with a 1.3 % yield...), while simultaneously providing a substantial income stream.

This outcome stems from the portfolio’s core construction. The focus on high, stable income from value-oriented assets meant it could not fully capture the sharper growth momentum that propelled the broader MSCI World index to +16.57%. This is an inherent trade-off: the strategy prioritizes income resilience and lower volatility, accepting that it may not fully participate in the strongest phases of a pure growth rally. The goal is simple: generate high income, independent of market swings.

B/ The yield is high, but the portfolio is not diversified enough

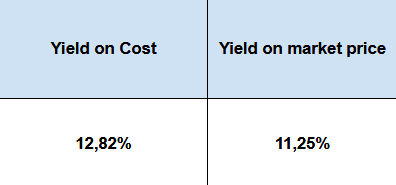

Let’s be precise: the yield on cost stands at 12.82%, while the current yield based on market prices is 11.25%. The 12% yield in the title is a rounded average that clearly reflects the portfolio’s income strength. This difference is a positive sign, reflecting both the powerful effect of dividend reinvestment and the capital appreciation of the holdings. The current yield of 11.25% remains highly compelling for an income-focused strategy. The main challenge, however, will be to secure this high level of income by enhancing portfolio diversification. Therefore, the key priority for the coming quarters is to broaden the portfolio’s base while preserving its strong income-generating capability.

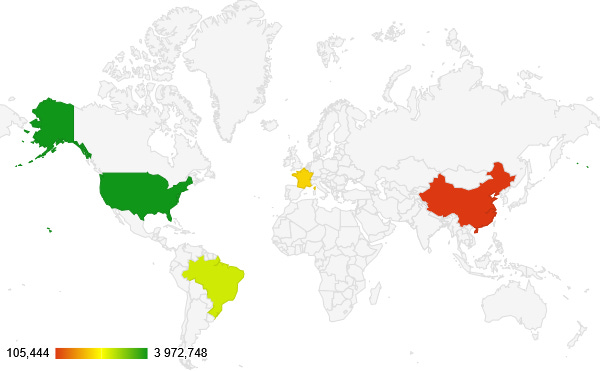

The map below reveals a significant concentration of investments in just four countries: the United States, Brazil, France, and China. While a global ETF has been added to the portfolio to mitigate this risk and improve geographic spread, its weighting is still relatively small.

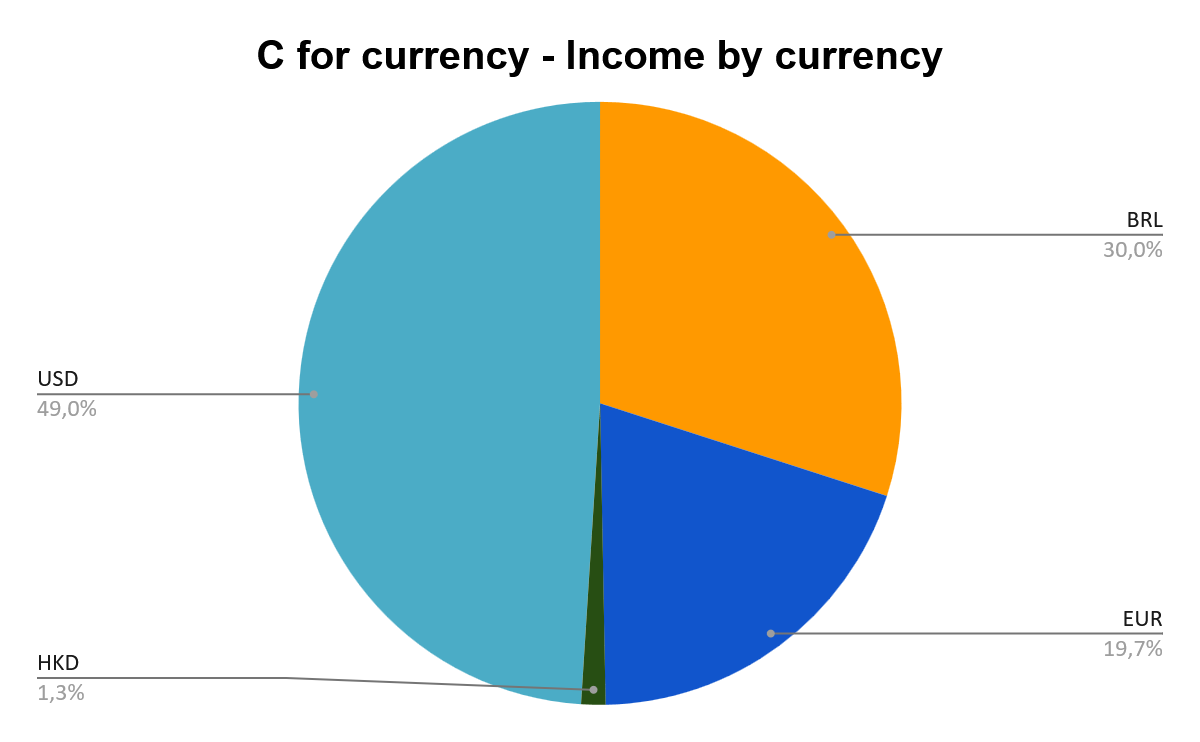

This income breakdown highlights a significant concentration, with the US dollar (USD) accounting for nearly half of all distributions (49.0%). The Brazilian real (BRL) and euro (EUR) represent 30.0% and 19.7% respectively, while the Hong Kong dollar (HKD) exposure is minimal at 1.3%. The target is clear: diversify into at least eight currencies, with no more than 30% in any single one, to secure income. Consequently, the focus for the coming quarters will shift decisively towards achieving this currency diversification, prioritizing risk management over pure performance.

This promising start demonstrates that high income and capital preservation are not mutually exclusive, yet the analysis clearly reveals that robust yield must be built upon a foundation of deliberate diversification rather than concentrated bets. This analysis confirms that diversification is the key priority. Now, let’s examine the individual components that have driven these results before outlining the path forward.

II/ Deconstructing the Holdings: Satisfactory Engine, Unfinished Chassis

A/ The Engine Room: Covered Call ETFs & Their Role: unstable and contracyclical income

The premiums are high when volatility is high. And volatility is high in bear markets: that is why covered call ETFs are contracyclical. Among the income-oriented ETFs in the portfolio, JEPQ, XYLD, and JEPG provide regular monthly distributions. JEPQ has been the most rewarding so far, not only delivering consistent income but also generating meaningful capital gains this year. By contrast, XYLD appears less compelling, as its performance has lagged and its high distributions suggest overpayout, raising questions about long-term sustainability. JEPG, meanwhile, is both a recent addition to the portfolio and a relatively new ETF in the market. While its current yield of around 8% is somewhat modest compared to the portfolio’s overall income target, it offers diversification and a more balanced approach. For this reason, I plan to build up JEPG gradually and in measured doses, ensuring that exposure remains disciplined so as not to dilute the portfolio’s strong income profile.

That said, covered call ETFs do their job—monthly income—but they can’t be the only source. They remain heavily concentrated in U.S. equities, and there is an inherent risk for investors who lean too heavily on option premiums without sufficient diversification among income sources.

B/ Core Equity Holdings: Getting Paid for Volatility

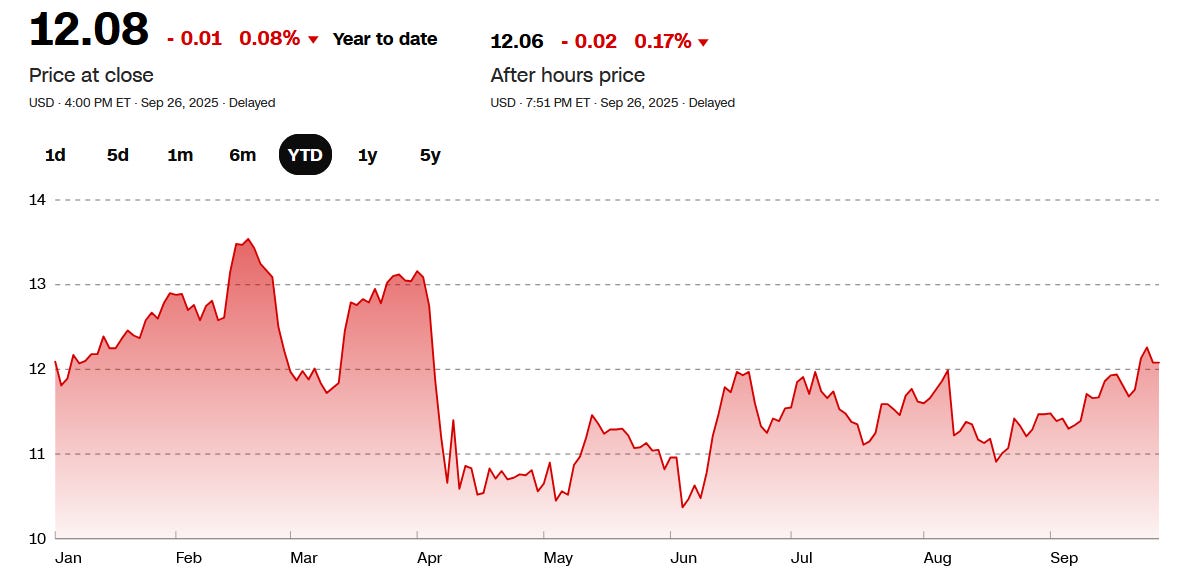

Petrobras—specifically its preferred shares, which are held to maximize yield—continues to be a high-risk, high-reward component of the portfolio. The stock exhibits significant volatility, as shown below, yet it generates substantial dividends. The price fluctuates between $10 and $14, but I accept that volatility because it is offset by a double-digit dividend.

Icade exhibits a comparable profile: it offers a high dividend, but its share price is highly volatile, typically trading in a range of €18 to €24. I have no regrets about this holding; the volatility is more manageable within the context of a bull market. Ultimately, I am compensated for holding through the price swings.

The income mechanism differs: covered call ETFs provide a premium derived from volatility, whereas stocks like Petrobras and Icade pay a dividend that compensates me for enduring their price swings. Crucially, the collective dividends have provided the capital to fund new investments.

C/ Fueling Growth: How Dividends Fund New Diversification

All portfolio income is being directed towards new, high-yield investments for diversification: Banco do Brasil, Edvantage, and JEPG (for the last 3 months). I initially intended to buy Best Pacific International Holdings, but the price rose too quickly. Furthermore, my broker paid my Icade dividends quite late, so by the time the funds arrived, the price was already too high. The stock remains on my watchlist, pending a price pullback.

In any case, I have successfully achieved sectoral, geographic, and currency diversification without reinvesting a single cent of new capital. This is the core concept of the portfolio. Next dividends will be used to invest in Legal and General.

Source: https://finance.yahoo.com/quote/2111.HK/

The analysis of the current holdings confirms the portfolio’s income strength but also its key vulnerability. The path forward, therefore, is clear: systematically execute the diversification plan without compromising the high-yield objective while anticipating megatrends and applying I-CASH method.

III/ Perspectives

A/ All the Mega trends are not covered yet

Six major megatrends were identified. The portfolio has begun to address four of them. The first is the Geo-Economic Shift – the transfer of wealth creation towards Asia – which is captured by our initial investments in the region. The second is Currency Risk, which we are tackling through increased diversification, though this effort remains a work in progress. The third, Technological Disruption and the rise of AI, is represented by our exposure to the Nasdaq. Finally, the Energy Transition is addressed through our position in Petrobras, which reflects the impact of massive global energy investments.

However, two critical trends have not yet been incorporated: Demographic Shifts—specifically the economic effects of aging populations on interest rates and the demand for automation—and Geopolitical Risk, meaning the rising probability of global conflicts. The research has not yet been conclusive on this point. More precisely, given the stringent dividend yield requirement and current market conditions, no suitable candidate has clearly emerged to date. This remains an active area of focus.

Therefore, while the portfolio’s foundation is promising, the work is far from complete. The same applies to the full and systematic application of the I-CASH method, which will guide our future investments to ensure they are both strategic and disciplined. Remember: the I-CASH method is a disciplined investment filter focusing on Internationalization, Currency diversification, Asset class allocation, Sectoral balance, and High yield discipline.

B/ The I-CASH method is not fully respected yet

This is a fundamental and, ultimately, quite normal assessment. The primary challenge for the portfolio remains diversification. Its internationalization (I) is not yet complete, and its currency diversification (C) is similarly unfinished. In fact, whether concerning asset classes (A) or sectoral diversification (S), I have not progressed sufficiently to deploy long-term optimization techniques.

Indeed, once the portfolio’s deployment is more advanced, I will be able to optimize reinvestments in terms of currency exposure (based on forex market developments) and dividend yield. But that is another story. In the meantime, the snapshot representing the most accurate picture of the portfolio has evolved since the last portfolio update. Beyond the core trio of oil, real estate, and technology, the banking sector and private education have now joined to strengthen the income-generating engine.

Key lessons so far

High Yield and Appreciation Can Coexist: This case study proves that a ~12% yield can be achieved without sacrificing capital appreciation in a bull market, challenging a common assumption.

Diversification is the Non-Negotiable Foundation: The primary risk to a high-income strategy is concentration. Future success hinges on systematic geographic, currency, and sectoral diversification.

Income Fuels Its Own Growth: The portfolio’s core mechanic—using dividends to fund new investments—creates a self-sustaining cycle that reduces reliance on new capital.

A Strategy in Evolution: This portfolio is a living project: the framework is set (megatrends, I-CASH), now comes execution.

And, above all, income investing is powerful because it enables continuous reinvestment during the accumulation phase without requiring any new capital. If you want to follow how this high-yield portfolio evolves in real-time—with all its wins and lessons—subscribe today.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

Disclaimer: This article is for informational and educational purposes only and should not be considered financial or investment advice. The views expressed are solely those of the author and do not constitute a recommendation to buy, sell, or hold any security. Always conduct your own research and consult with a professional before making any investment decisions.