Are Petrobras Investors All Geniuses?

Spoiler: They’re just lucky. But luck pays the same as genius.

Petrobras is not a compounder: it is a distributor. A year ago today, I picked up 1,764 shares of PBR.A: the preferred ADR of Petrobras. Not long after, I published Are Petrobras Investors All Dumb?, a post that drew in new readers and, crucially, pushed me to truly unpack the company’s economic engine. Today, I genuinely love the position. And no, it’s not solely because the share price has skyrocketed. Let me walk you through the reasons.

I/ Shareholder POV: The Reasons Why They Can Feel Like Geniuses

A/ A Great 1 Year Price Return

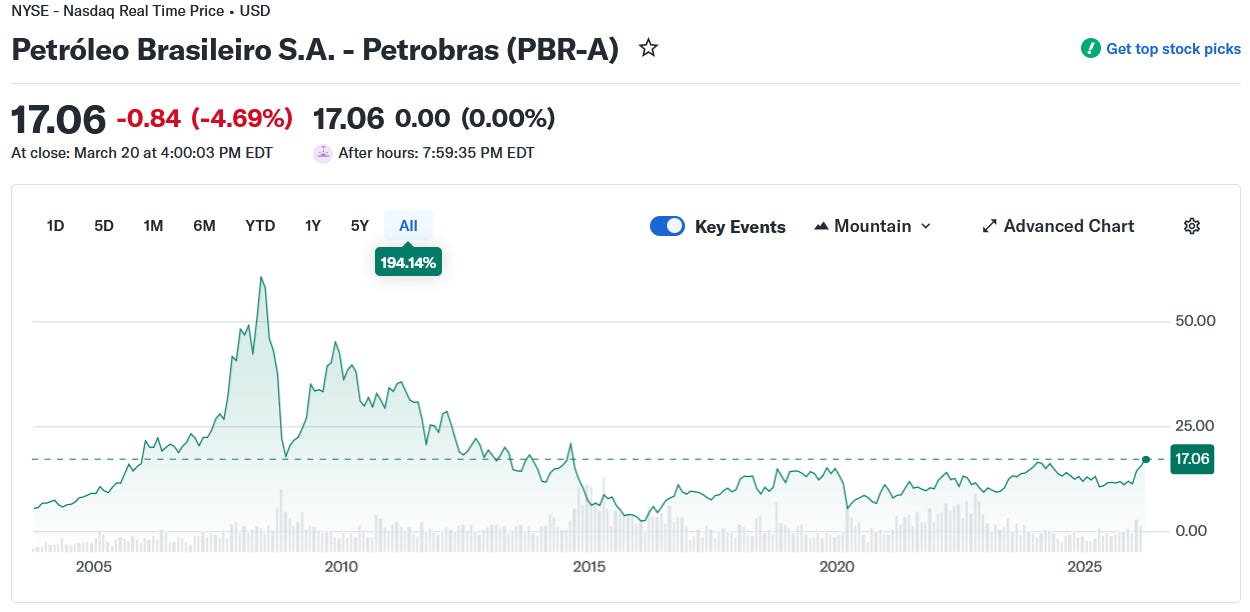

I bought shares of PBR.A at an average price of $11.69. From the outset, I knew the stock would be highly volatile, but I expected it to appreciate over the very long term. What I hadn’t factored in was the acceleration of geopolitical imbalances. As of March 20, 2026, after the market close, the stock sits at $17.06, for a gain of 45.94%.

Source: Yahoo Finance

Now let’s look at the “big picture”: volatility is in this stock’s DNA, exposed to market swings and political uncertainty, as we have repeatedly pointed out in various articles on Petrobras by Pipart Global Income. But focusing solely on the share price of a high-yield stock is somewhat superficial—if not outright dumb. It is probably time to turn our attention to the income.

Source: Yahoo Finance

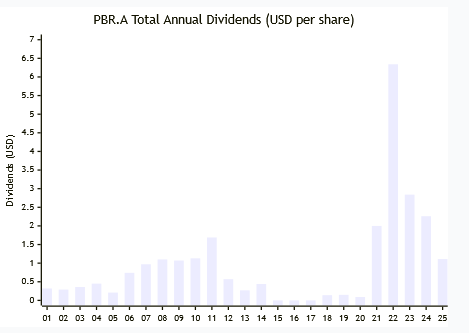

B/ A Cyclical Dividend Payment

As we have already observed in previous articles, dividend payments are cyclical and can even be interrupted for long periods. The year 2022 was exceptional, and the new dividend policy under the 2025-2029 plan (now extended and incorporated into the 2026-2030 Business Plan) is more reasonable and measured. It’s unfortunate for us as shareholders, but objectively, this makes the investment more sustainable and reasonable in the long term.

Key context: Petrobras’ shareholder remuneration remains tied to its policy of distributing dividends based on free cash flow (often around 45% in base scenarios), with a focus on financial discipline. The 2025-2029 plan projected ordinary dividends of roughly $45-55 billion over the period (with flexibility for extras), but revisions in the 2026-2030 plan slightly lowered expectations (e.g., $45-50 billion ordinary, no mention of large extras), reflecting lower oil price assumptions and a priority on debt control, capex efficiency, and long-term resilience rather than aggressive payouts.

This shift away from the ultra-generous 2021-2022 levels (driven by the oil super cycle) toward a more conservative, predictable regime is indeed a trade-off: lower near-term yields for most shareholders, but reduced risk of suspensions or volatility in tougher cycles ahead.

Based on the projected average annual dividend of $1.40 to $1.55 per ADR under Petrobras’ 2026-2030 Business Plan, the yield on cost (at my average purchase price of $11.69 per ADR) falls in the range of 12.0% to 13.3%, while the yield on market (at the March 20, 2026 closing price of approximately $17.06 per ADR) would be in the range of 8.2% to 9.1%. In short, Petrobras transitioned from High Yield / High Risk to Moderately High Yield / Moderately High Risk. For my cost basis, that is a compelling setup.

Source: Petrobras 2026-2030 Business Plan

C/ Total Return Is High, Which Is Nice for Income Investors

Since its NYSE listing in August 2000, Petrobras (PBR ADR) has delivered a strong cumulative total return (price appreciation plus dividends reinvested) of approximately +1,852% through March 20, 2026—turning a $10,000 investment into roughly $195,200. This represents a CAGR of ~12.3% annualized over roughly 25.5 years, according to totalrealreturns.com data. The S&P 500 total return over the comparable period has seen cumulative gains of around +630% (CAGR of ~8–9% annualized from 2000 to early 2026), accounting for the dot-com bust, 2008 crash, and subsequent bull markets.

Shorter horizons highlight PBR’s extreme volatility: 5-year total return ~677–698%, 10-year ~1,499%, and for the PBR.A variant, 20-year ~413%. These results are often driven by massive dividend payouts during oil super cycles (e.g., 2021–2022), contrasted with deep drawdowns (>80–90% in crises like the 2014–2016 Lava Jato scandal and COVID). In contrast, the S&P 500’s more stable profile (e.g., 20-year ~622%, 10-year ~272%) reflects broad-market compounding with lower risk.

Overall, PBR has rewarded patient, risk-tolerant investors with superior long-term returns since inception, but its cyclical, geopolitically exposed nature means outperformance comes with far higher volatility than the diversified benchmark, proving that in this case, “luck” (timing oil booms and high payouts) has indeed paid as well as genius. For context, my own total return—price appreciation plus dividends received—stands at 60% over the past year, a reminder that in a high-yield stock, the income component matters as much as price appreciation.

Among these otherwise appealing features, there remains one downside: the withholding tax on dividends for non-residents has been reintroduced. It’s a regrettable but not entirely unexpected situation. That said, given that a significant share of payouts is already made via JCP, which are taxed as interest and subject to a 15% withholding tax, this new measure doesn’t alter things substantially.

II/ Business Holder POV: The Fundamental Reasons Why I Remain Humble and Hold for the Very Long Term

My investment horizon is simple: I’d like to pass these preferred shares on to my children when I pass away. That changes everything.

A/ The Best News: Oil Production Has Clearly Increased

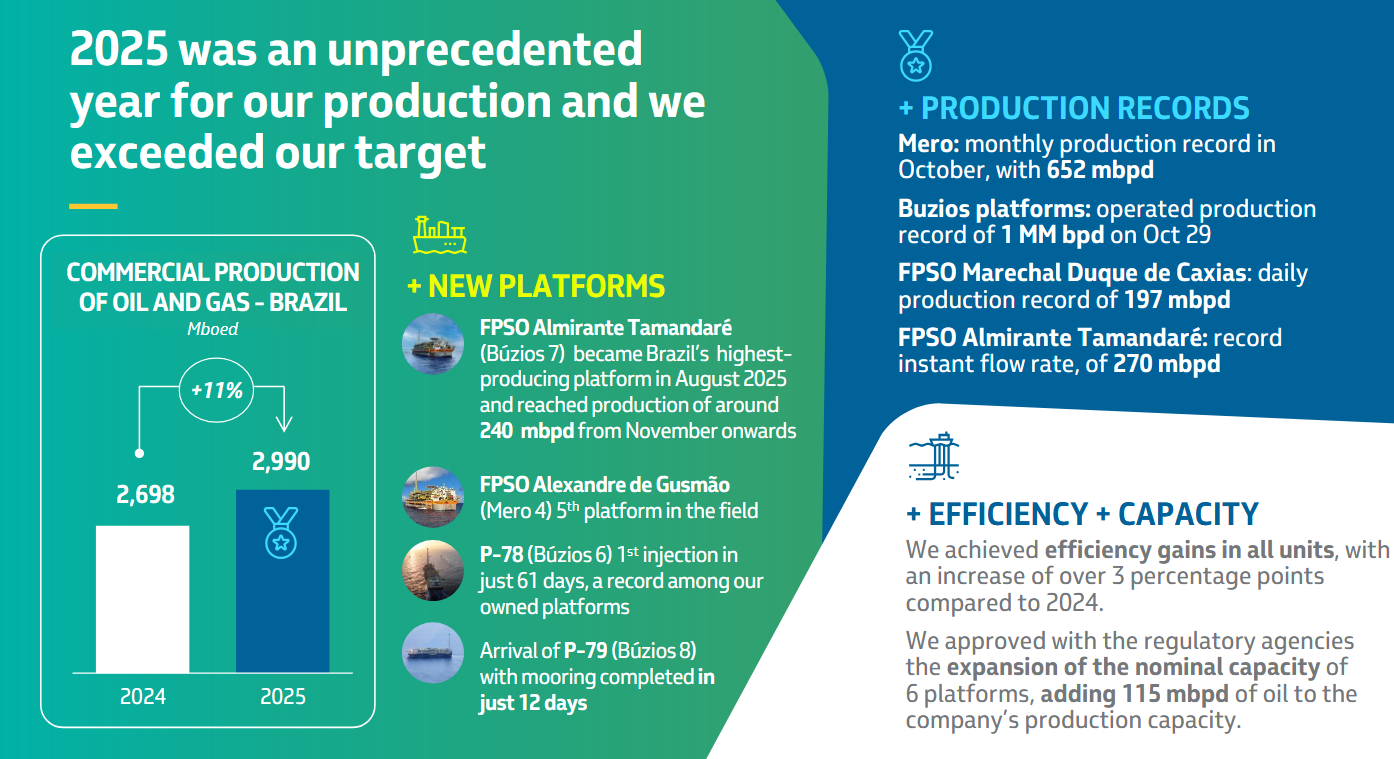

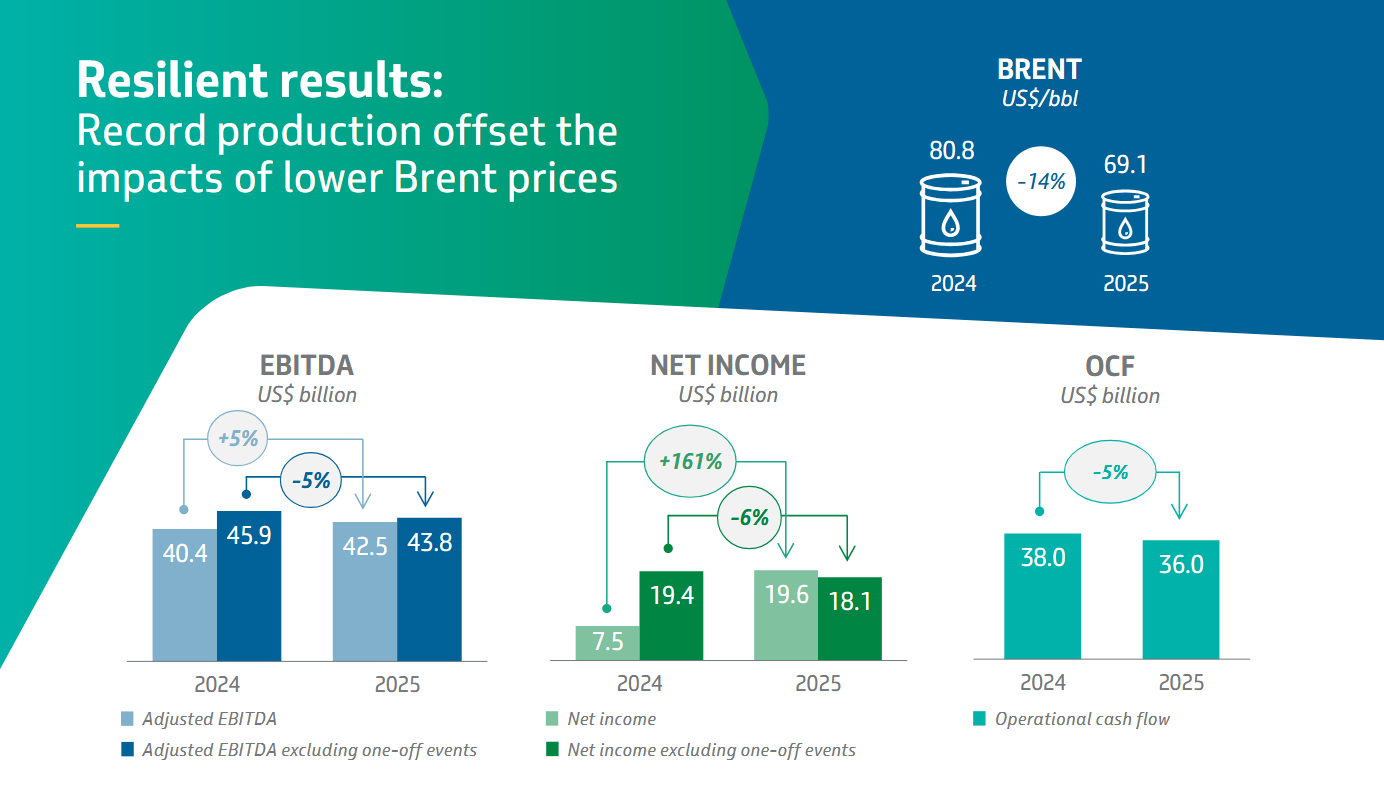

In 2025, Petrobras delivered outstanding operational performance, increasing its commercial oil and gas production in Brazil to 2,990 mboed, up 11% year-on-year and exceeding the upper end of its guidance. This growth was driven by the ramp-up of high-capacity FPSOs in core pre-salt fields such as Búzios and Mero, alongside record production levels and improved operational efficiency.

Pre-salt assets—now accounting for roughly 82% of total output—continue to underpin Petrobras’ low-cost, high-volume growth strategy. On a global scale, with oil supply around 100–102 million barrels per day, Petrobras produced approximately 2.4 million barrels per day of oil (and ~3 mboed including gas), representing ~2.3–2.5% of global supply and reinforcing its position as a leading non-OPEC producer.

Source: Petrobras Operational Report 2025

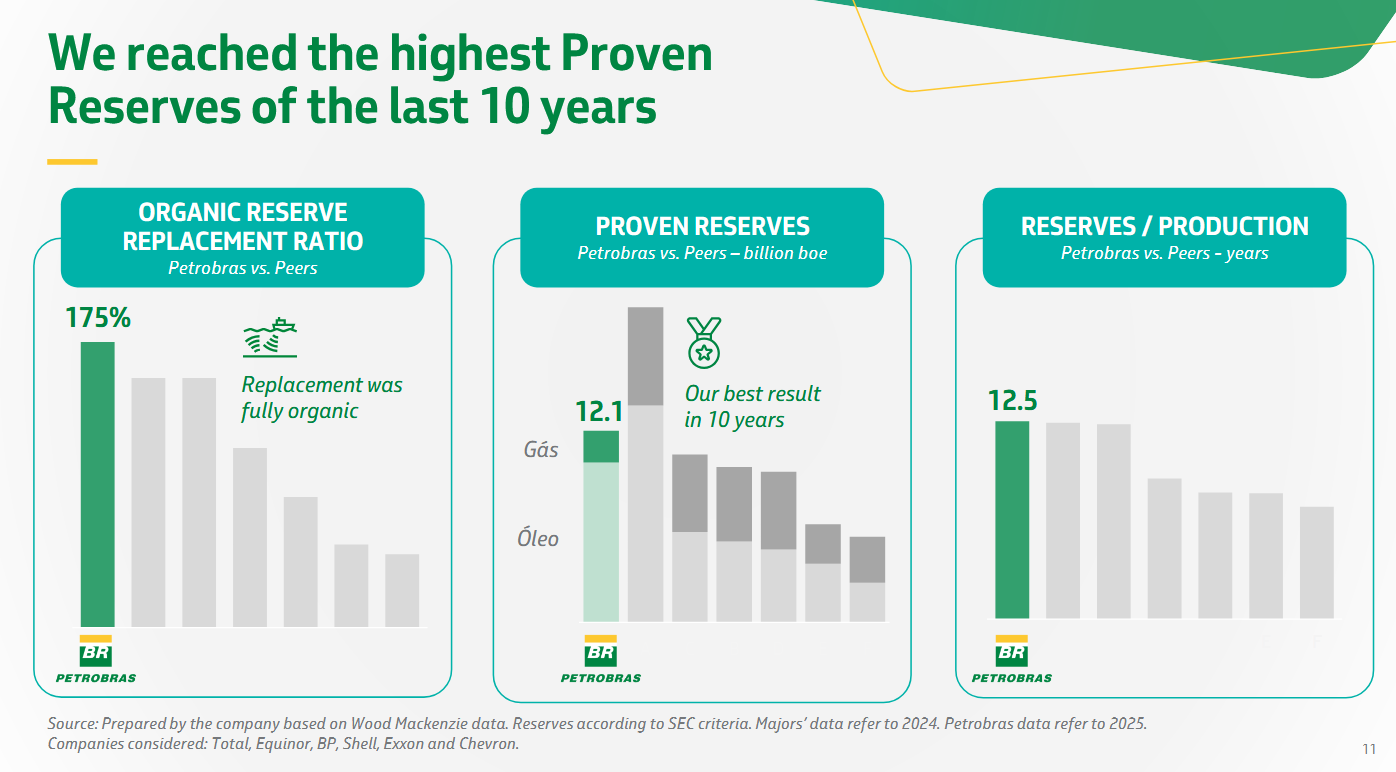

In 2025, Petrobras reached its highest proven reserves in a decade, at around 12.1 billion barrels of oil equivalent (boe) (SEC standard). More importantly, the company replaced significantly more oil than it produced, with a reserve replacement ratio (RRR) of 175% —entirely organic—adding 1.7 billion boe despite a year of record production.

This results in a reserves-to-production (R/P) ratio of ~12.5 years, meaning Petrobras could sustain current output for over a decade without new discoveries. Compared to peers, Petrobras stands out:

ExxonMobil: strong RRR (often >100%), R/P ~13 years

Chevron: ~158% RRR, but shorter R/P (~8–10 years)

TotalEnergies: ~115–157% RRR, R/P ~12 years

Shell: weaker RRR (~85%), R/P ~9 years

BP: ~90% RRR, R/P ~7–8 years

While some majors hold larger absolute reserves, Petrobras delivers one of the strongest organic renewal profiles in the sector, driven by its high-quality, low-cost pre-salt assets.

Why this matters: high organic reserve replacement—especially in low-cost fields—directly supports future cash flow visibility. In other words, Petrobras is not just replacing barrels, but replacing profitable barrels, which underpins its ability to generate sustainable free cash flow over time.

Source: Petrobras Operational Report 2025

B/ Financial Environment Is Nice: Debt, USD/BRL, Leverage, FCF

The financial environment remains supportive across key metrics.

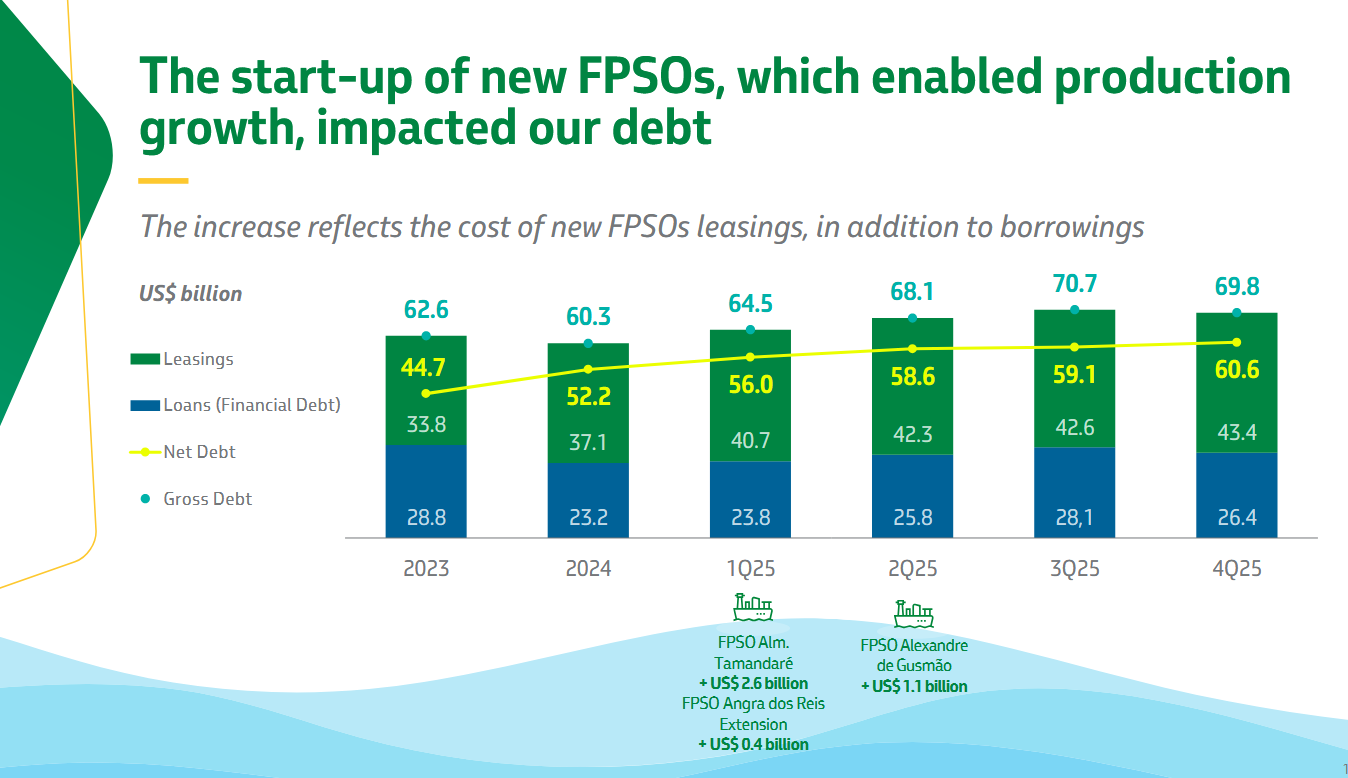

Debt & Leverage: Net debt stands at $60.6 billion with a healthy net debt-to-EBITDA ratio of 1.42x—well below the 2.5x internal ceiling, reflecting moderate leverage and ample headroom.

Sources: Petrobras Financial Reports

FCF & Levered Cash Flow: Despite elevated capex of $20.3 billion in 2025, Petrobras generated robust FCF of ~$16.7 billion, highlighting the cash-generating power of its low-cost pre-salt base. After years of aggressive deleveraging, financing costs are well under control, meaning levered cash flow translates efficiently into cash available to shareholders. In practical terms, a large portion of this free cash flow remains available after debt servicing, making it a reliable proxy for distributable cash to equity holders. Compared to peers, Petrobras stands out for combining high FCF generation with low financial pressure—a strong foundation for sustaining shareholder distributions.

USD/BRL Dynamics: The USD/BRL rate (~5.32) remains a structural tailwind. With 70–80% of revenues in dollars and a significant portion of costs in reais, Petrobras benefits from a natural hedge that bolsters cash flow and dividend capacity.

👉 Bottom line: Beyond operational strength, Petrobras’ financial setup (low leverage, strong levered cash flow, and favorable FX dynamics) reinforces its ability to generate and distribute cash over the long term.

Sources: Petrobras Financial Reports

C/ The Business Strategy Seems Well Executed

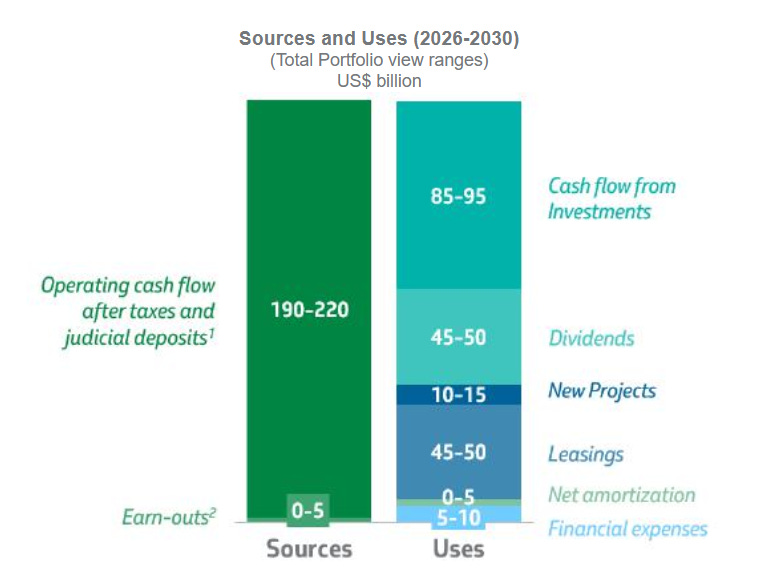

Strategically, Petrobras has finally found a groove that makes sense. The focus is clear: maximize value from the pre-salt crown jewels while maintaining capital discipline. The 2026-2030 Business Plan reflects this balance—capex is directed primarily toward high-return offshore projects (with ~70% allocated to exploration and production), the dividend policy has become more predictable, and the company has shown restraint in pursuing the kind of empire-building that plagued it in the past.

Source: https://petrobras.com.br/en/quem-somos/estrategia

On execution, the track record speaks for itself. Production exceeded guidance in 2025. Reserve replacement is best-in-class. Costs remain among the lowest in the industry. These aren’t signs of a company coasting—they’re signs of a company executing well on a sensible plan.

Now, we won’t dwell further on the elephant in the room. That’s political risk. It remains high in Brazil, but that’s the price of investing in this company. I’ve accepted being in partnership with the Brazilian state... and I’m keeping my fingers crossed.

What I can control is my time horizon. And for a very long-term holder, the gap between a well-executed strategy and a volatile political environment creates exactly the kind of opportunity I’m willing to live with.

Investor Takeaway: Thesis Unchanged, but Now Price Supports It

With the stock now trading at a level that better reflects its fundamentals, my conviction remains intact. Petrobras remains a great investment for the very long term. Over the past year, I’ve appreciated this investment because it has delivered on its promises: high volatility, strong dividends, and real but well-identified risks. The biggest risk remains political risk, but that’s just how it is. In any case, I’ve achieved a 60% total return over one year (PBR.A shares bought at $11.69).

As a long-term investor, I see solid reserves, a strategy that seems reasonable to me, and reasonable income prospects. I’m comfortable with that. It’s not perfect—I had hoped for even higher income and lower taxes—but the trade-off remains favorable. I like this company and its business model, so I’ll continue to monitor its evolution. It’s more engaging than watching a covered call ETF, and the capital appreciation prospects are significantly better, though it does require more time and attention.

This position is already large enough in my portfolio, so I’m letting it ride and reinvesting the dividends elsewhere. I won’t add at these levels—but let’s revisit that in a few quarters.

In short, Petrobras is not a compounder: it is a distributor.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.