Double Digit Yield in Germany?

Is the new DYLD ETF an option?

It’s been a long time since I’ve been looking for a tool to generate income in euros and on German stocks. I’ve found one, and I’d like to put it under the microscope. Even if it won’t be a core investment, every line counts in income investing. Above all, I want to diversify my portfolio by adding euros, industry exposure, and a developed country with long-term potential. I know my investment thesis (European diversification) is relevant, at least at this stage of my portfolio’s development.

I/ Investment Thesis: Why the DAX Is a Good Long-Term Diversification Candidate in an Income-Oriented Portfolio

A/ The DAX: A High-End “Industrial ETF” Paid in Euros

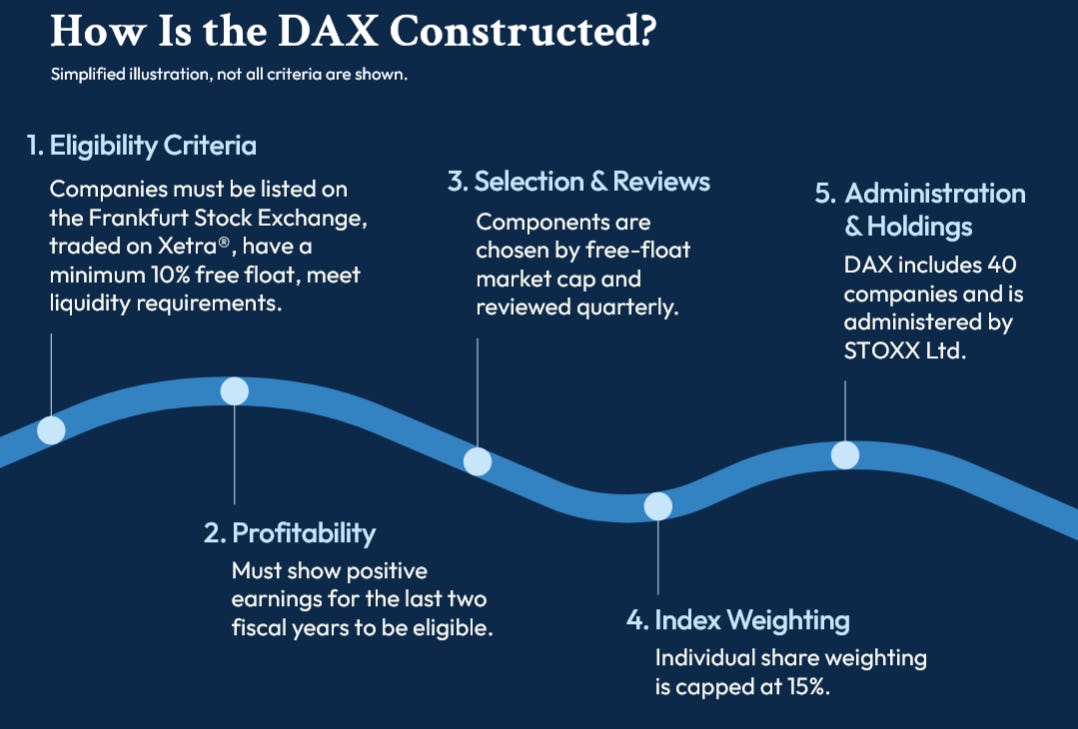

Not quite. But let’s start with the basics: the DAX (Deutscher Aktienindex) is Germany’s flagship stock market index, representing the 40 largest companies listed on the Frankfurt Stock Exchange. It is managed by STOXX (a subsidiary of Deutsche Börse) and is often compared to France’s CAC 40 or the U.S. S&P 500. Adding a slight technical note: the DAX is a total return index (dividends are reinvested in the index). It is weighted by free-float-adjusted market capitalization, meaning company weights are based on the value of shares available on the market, excluding stakes held by founders or the state. A capping rule limits any single stock’s weight to 15% of the index.

Source: Stoxxx

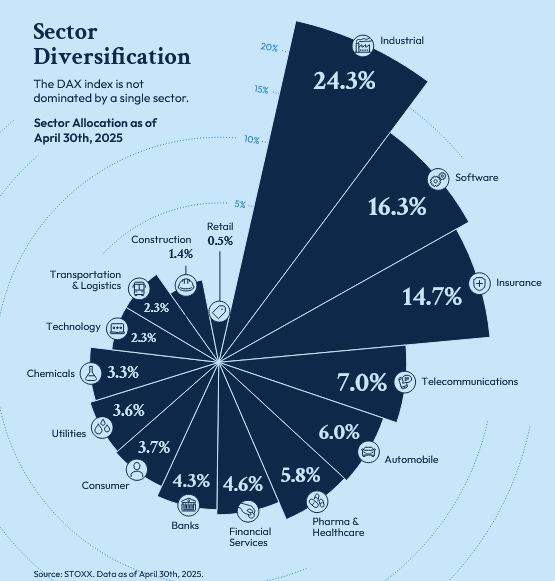

So what’s in it? The DAX is indeed a “predominantly industrial ETF.” The data highlights this: if we add the strict industrials sector, chemicals, and automobiles, industry accounts for about one-third of the index. Thus, the DAX is largely export-oriented and dependent on the global economic cycle. That’s the first theoretical lesson: it’s a cyclical index.

Source: Stoxxx

B/ Volatility Is the Price to Pay for the Privilege of Holding the DAX

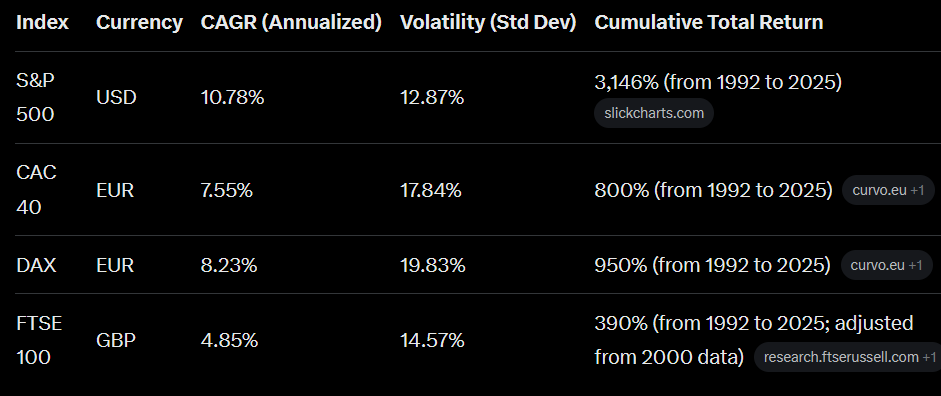

This observation is confirmed by results: the DAX’s volatility has been higher over the long term than that of the S&P 500, CAC 40, or FTSE 100. It’s a cyclical, volatile index that delivers very strong long-term performance (8.23% from 1992 to 2025). As the comparison shows, the DAX outperforms other major European indices in total return and has a standard deviation—the best metric for calculating volatility—of 19.83%, well above that of other major developed-country indices.

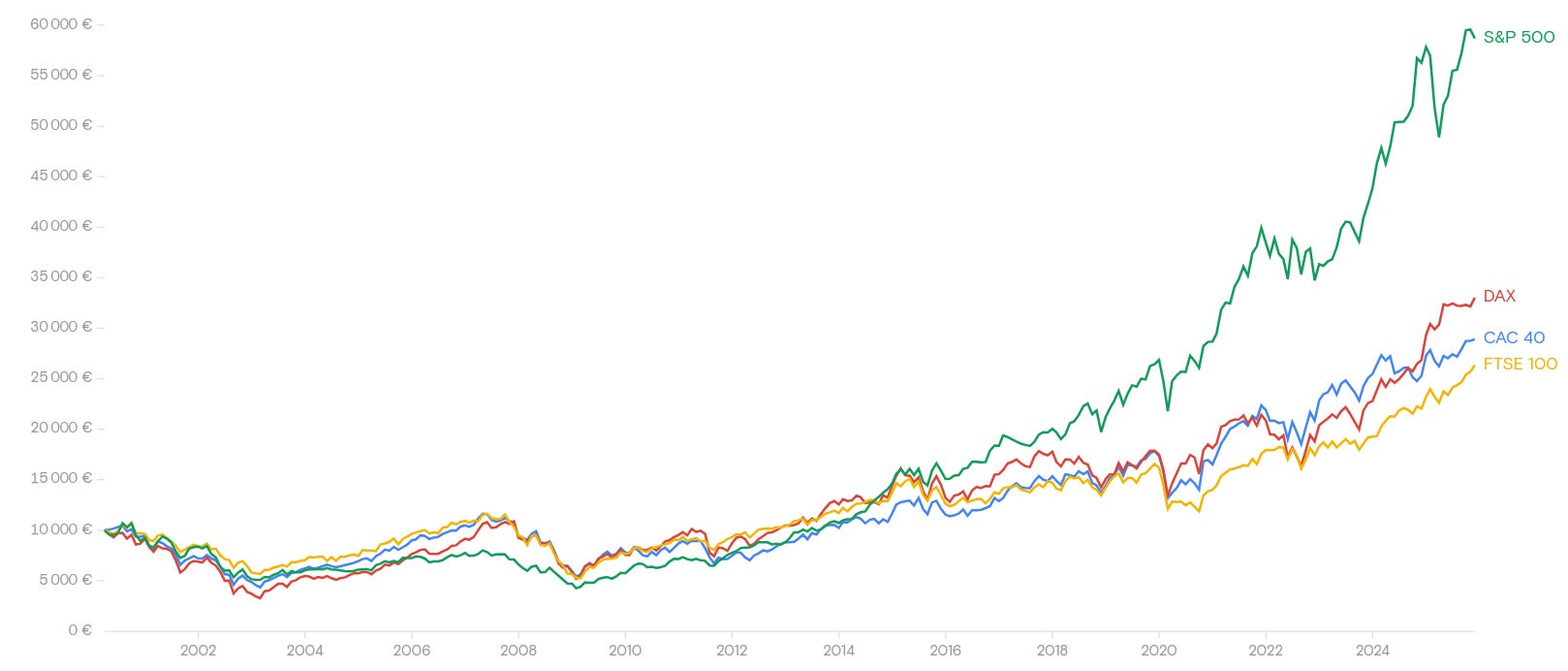

At this point, we can confidently state that the DAX is essentially an industrial, cyclical, volatile vehicle featuring world-class international companies. The performance comparison provides a fairly precise overview.

Source: Curvo

C/ The DAX: A Romantic Choice, Not Really an “Income-Oriented” One

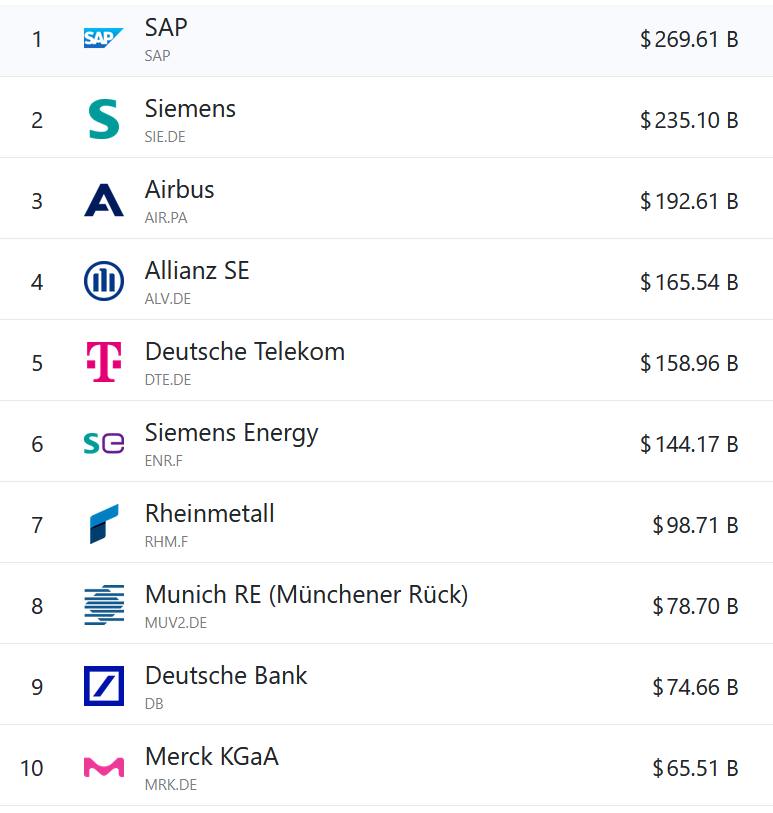

The DAX, we haven’t said yet, is an assembly of brilliant global brands. Let’s focus on the top 10, which account for about 64% of the index’s capitalization. Anyone who’s worked in a large company knows SAP is pretty much unavoidable, knows Siemens, Airbus, Allianz (one of the world’s best insurers), Deutsche Bank, etc. Not to mention the world’s top automobile brands like BMW, Mercedes-Benz Group, or Volkswagen. These are historic, excellent, and essential companies. Owning them is a quality guarantee for your portfolio. In short, it’s a concentrated—perhaps overly concentrated—package of excellent companies. This concentration increases volatility but provides assurance of investing in strong businesses. These are rational good bets.

Source: https://companiesmarketcap.com/dax/largest-companies-by-market-cap/

It is also an emotional bet. We should never underestimate this aspect, as it is inherent to a relatively good knowledge of the country and the ability to hold an investment long-term. Germany is the land of so many great thinkers, from Goethe to Hegel, of an unquestionably superior work ethic compared to the global average, and a country for which I have affection, having personal German roots. BUT it is clearly not the temple of income-oriented investing.

Indeed, the average dividend is low (around 2.5%), and taxation is often high: 26.5% withholding tax for non-residents before double tax treaty. Even reduced to 15%, you’ll need a more financially and fiscally efficient vehicle to generate substantial income from the German market. The DAX is therefore not an “income temple,” but an excellent candidate for European diversification in euros, provided it’s dressed with an appropriate strategy. That’s exactly what the tool I’ve identified allows, which we’ll scrutinize in the next section. And, facing a volatile index with long-term growth, the covered call tool seems quite suitable. In other words: it’s an excellent underlying poorly exploited by dividends alone.

II/ Investment Vehicle: Is DYLD (Global X ETF) a Good Choice?

First, for those who don’t know how covered call strategies work, it’s worth understanding the basics: these strategies involve selling call options against a portfolio you own, generating premium income in exchange for capping your potential upside. It’s a trade-off between regular income and unlimited growth potential. Read this for further information: Are Covered Call ETFs a Scam? Part 1 - XYLD - Pipart Global Income 10%+ Yield.

A/ There Are Many Reasons Not to Invest Right Now

Structural Flaws

What I really don’t like: it’s a synthetic replication ETF. Unlike physical replication where the fund holds the DAX stocks directly (or nearly), DYLD uses a synthetic approach via an unfunded swap with a counterparty (usually a bank). In short: the ETF doesn’t buy the DAX stocks; it enters into a derivative contract promising to pay it the index performance (price + dividends adjusted for the covered call strategy) in exchange for remuneration. Counterparty risk is therefore real: if the bank defaults (bankruptcy, etc.), you could lose part or all of your exposure, even if collateral (often high-quality assets) is supposed to limit it to 10% max per counterparty under UCITS rules.

For an “income” product like this, which aims for stability and regular distributions, I find it frustrating: we take additional risk (counterparty + swap complexity) for a strategy that’s already not straightforward during periods of high volatility or strong bull markets (where sold calls cap gains).

Current Market Drawbacks

The DAX price is quite high at the end of January 2026. For a global long-term investor, it’s not the only issue. But we need to keep it in mind.

Source: World PE Ratio

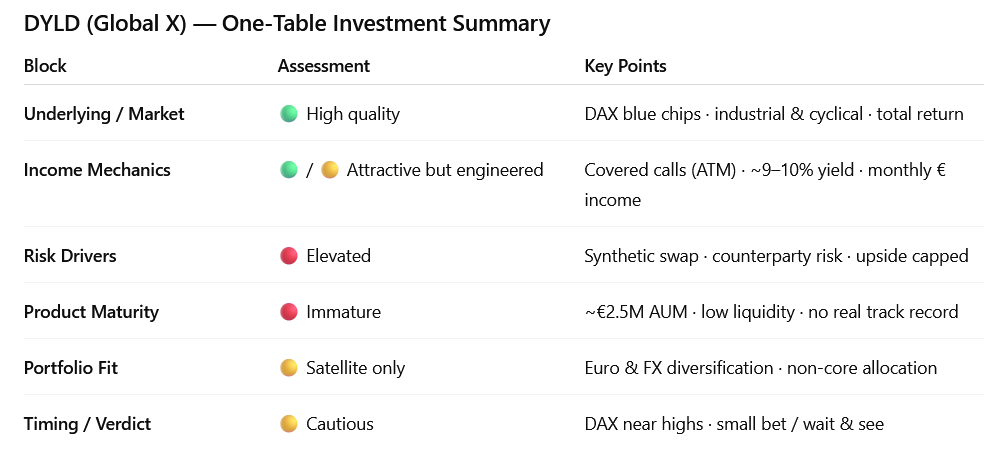

Moreover, the product is very recent. DYLD was created in November 2025 (official launch on November 25, 2025 on Deutsche Börse Xetra) and its assets under management are very limited. As of end-January 2026 (latest data around January 30), the fund’s AUM stands at about 2.5 to 3 million euros according to sources. It’s tiny for a UCITS ETF, especially compared to European covered call giants (e.g., the Global X QYLD suite totals several hundred million, and the UCITS covered call market exceeds 4-5 billion globally).

This small size poses several concrete problems: low liquidity with potentially wide bid-ask spreads (even if reasonable on Xetra for now), modest daily trading volumes (tens/hundreds of thousands of euros), and higher risk of NAV discount/premium in stress. There’s also a risk of premature closure: small ETFs (under 10-20 M€) are often “at risk” with issuers; if inflows don’t take off quickly, Global X could merge or liquidate it in 1-2 years (classic for niche launches like this on the DAX). Finally, there’s a complete lack of history: zero real track record beyond 2 months makes it impossible to assess how the ATM covered call strategy on DAX behaves in a true bear market, volatile sideways movement, or strong rally (sold calls cap upside, but do collected premiums really help?).

It will therefore be a diversification line and not a core line. But it remains very important.

B/ But the Promise Appeals to Me Too Much to Resist

Among UCITS covered calls, DYLD stands out as one of the very few purely European products (domiciled in Ireland, UCITS-compliant, listed on Deutsche Börse Xetra in euros, and specifically targeting German/European investors via the DAX). Unlike most covered call strategies available in Europe (often UCITS versions of QYLD/XYLD on Nasdaq/S&P 500, thus exposed to the US dollar), DYLD offers direct exposure to the DAX while generating income via monthly ATM option premiums sold.

The real plus for European income investors: recurring income in euros (monthly distributions, forward yield estimated at ~9.7% according to DivvyDiary), avoiding the double penalty of euro-dollar exchange. Many income portfolios are overweight in dollars (via QYLD, US JEPI-like, or American dividend aristocrats), exposing them to significant currency risk when the euro strengthens or the Fed cuts rates faster than the ECB. DYLD allows diversifying this monetary concentration while maintaining a high-yield income strategy: option premiums boosted by European volatility, exposure to solid sectors (industrials ~35%, finance ~19%), and potential for overall portfolio volatility reduction thanks to the buy-write strategy.

Source: https://globalxetfs.eu/funds/dyld/

In summary, the key figures as of January 30, 2026 are correct on paper (low TER, clean UCITS structure), but the tiny AUM of 2.55 M€ and the age of 2 months make DYLD still too risky for a serious allocation. It’s a promising product on paper (high yield in euros, DAX exposure), but we need to wait for it to reach at least 20-50 M€ and 12-18 months of life for liquidity, stability, and track record to become convincing. For now, it’s pure “wait and see”—or a small speculative bet for those who strongly believe in the rise of European covered calls.

Source: https://globalxetfs.eu/funds/dyld/

Investment Takeaway

I want to be among the early adopters of this ETF and accept the risks. Concretely, I’m going to buy some in the coming days with the next distributions I’ll receive. A small position to monitor, with the hope that the income investing market finally unlocks in Europe.

As you’ve seen, not everything is totally rational in this choice: I love German exporting companies, and I believe its economic and financial genius will allow it to reposition on international markets, whatever the sector. It won’t be a core investment, but a good tool for geographical and currency diversification that, I hope, will perform over the long term.

In short, I’m dipping a small toe into DYLD, Global X’s new DAX Covered Call ETF (9.7% forward yield in euros). It’s one of Europe’s rare high-income plays on German blue-chips, perfect for euro diversification away from dollar-heavy portfolios. But it’s tiny (€2.55M AUM), synthetic (counterparty risk), and brand new (launched Nov 2025)—pure early-adopter speculation. Worth watching if European covered calls take off?

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

There is also a Eurostoxx Covered Call ETF from Global X that is already six months old, with AUM of >€50 million. I am curious to see how it performs compared to the DAX ETF.