Is Private Credit a Terrible Idea for Income Investors?

Are Bdcs Investable Anew?

An income investor must diversify the income sources throughout the economic cycle. And to maintain a high yield, they must constantly hunt for sectors or regions offering elevated dividends that are currently trading at a discount.This raises two key questions: first, what role do BDCs play in a global income portfolio in general?

And second, more specifically, what role could they play for me right now, at a time when everyone is talking about private credit as a potential source of systemic risk? Most investors will avoid BDCs today because of fear. That’s usually when they become interesting.

I/ How to Incorporate BDCs into an Income Investing Strategy

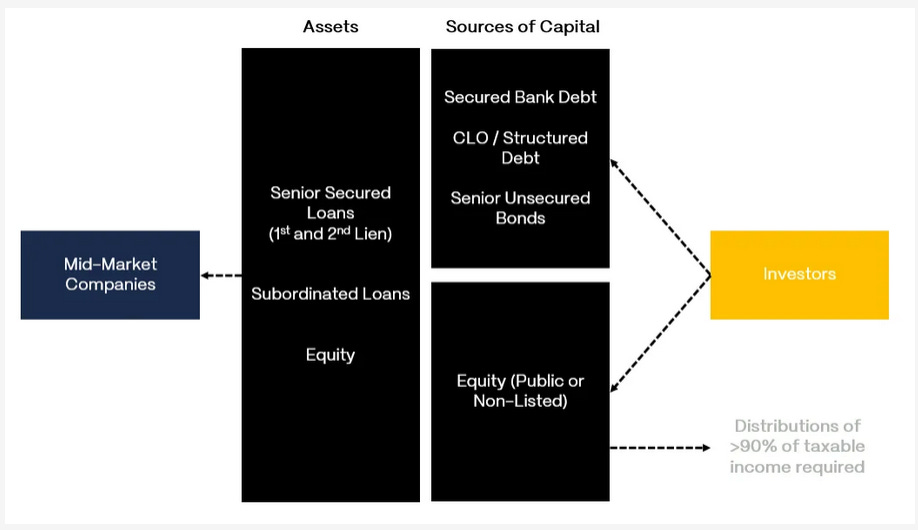

A/ How a BDC Works: A Bridge Between Savers and Real Businesses

A Business Development Company (BDC) is a clever financial intermediary that connects everyday investors with mid-sized American companies that traditional banks often overlook.

Here’s how it works in four straightforward steps:

It raises capital from investors – Anyone can participate by simply buying shares of a publicly traded BDC on the stock exchange, just like buying Apple or any ETF.

Your BDC deploys that capital into real businesses: the BDC lends money primarily to middle-market companies (typically those with $10M to $250M in revenue) in the form of senior secured loans. These loans are backed by the company’s assets and sit at the top of the capital structure, meaning they get repaid first if things go wrong. Most carry floating interest rates (usually SOFR + a 4–7% margin).

Your BDC earns attractive interest income: Thanks to the credit risk premium and the illiquidity of private lending, BDCs typically generate gross yields between 9% and 12%+, sometimes higher depending on market conditions.

It passes nearly all of that income to you for tax reasons: BDCs are required to distribute the vast majority of their earnings as dividends, often delivering 8-14% annual yields to shareholders.

Source: junkbondinvestor

Why are dividends so high?

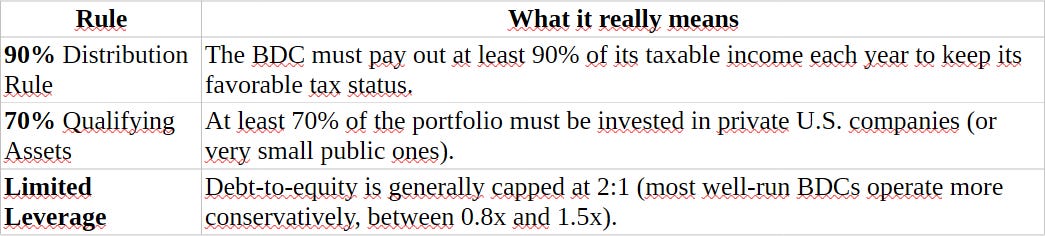

BDCs benefit from a special tax status called RIC (Regulated Investment Company). If they distribute at least 90% of their taxable income each year, they pay virtually no corporate tax. The income flows straight through to investors – tax-efficiently at the fund level.

The Three Golden Rules of BDCs: Remember These

There’s also an important soft rule: BDCs don’t just lend money – they must provide significant managerial assistance to the companies they finance (strategic advice, board seats, operational support). It’s lending with a hands-on approach.

In short, a BDC is essentially a publicly accessible loan fund that provides senior secured financing to mid-sized businesses and rewards investors with high, regular dividends – in exchange for taking on moderate credit risk rather than pure equity volatility.

B/ How a BDC fluctuates during the Economic Cycle

1/ In Theory...

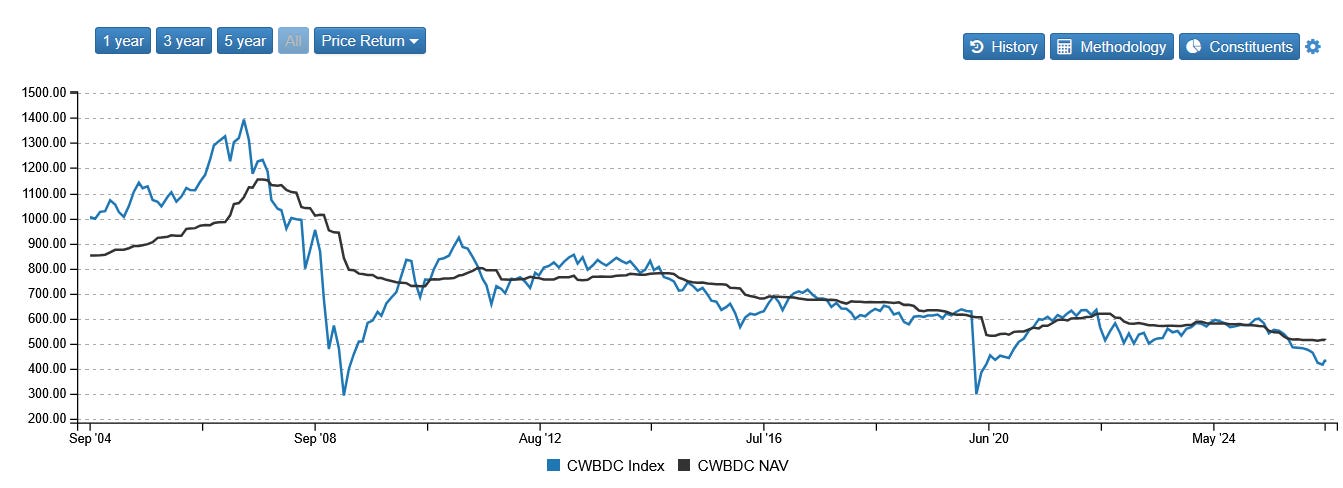

First, let us be purely formal and theoretical. The exercise is always worth doing. During economic expansions, BDCs see their net asset value (NAV) rise thanks to improving fundamentals of their portfolio companies (higher earnings, lower defaults). The market price often follows this increase, sometimes trading at a premium to NAV, reflecting investor optimism. In a slowdown or recession, however, defaults increase, leading to a drop in NAV and asset impairments. The market price can then disconnect and trade at a sometimes severe discount (10-30%), amplifying volatility. This decoupling between price and NAV offers opportunities for patient investors, but also signals credit stress.

BDCs are known for their high yields, often above 8-10%, but these are highly sensitive to the cycle. In growth periods, distributions are well covered by interest income and repayments, and the apparent yield remains attractive. When the economy deteriorates, BDCs may cut their dividends to preserve equity, which mechanically lowers the effective yield if the market price falls even faster. Conversely, at the cycle trough, the yield calculated on the discounted price can reach misleading highs (15-20%), signaling a high risk of further cuts. Thus, BDC yields are never guaranteed and reflect default expectations.

BDCs are not stocks. They’re floating-rate loan machines disguised as equities. In a global income strategy, BDCs offer a source of yield not perfectly correlated with government bonds or large-cap equities, thanks to their exposure to private credit in US SMEs. Their high income can usefully complement dividends from international stocks and coupons from high-yield bonds, potentially boosting a portfolio’s overall yield. That said, to manage the risks of discount trading and dividend cuts, some investors choose to allocate modestly (5-10%) and combine BDCs with other income assets like REITs, MLPs, or secured bonds. Keeping an eye on the NAV/price ratio and underlying portfolio quality can be helpful. When managed carefully, BDCs may serve as a dynamic addition for an investor seeking attractive income and cyclical diversification.

2/ In practice, market prices lead the game

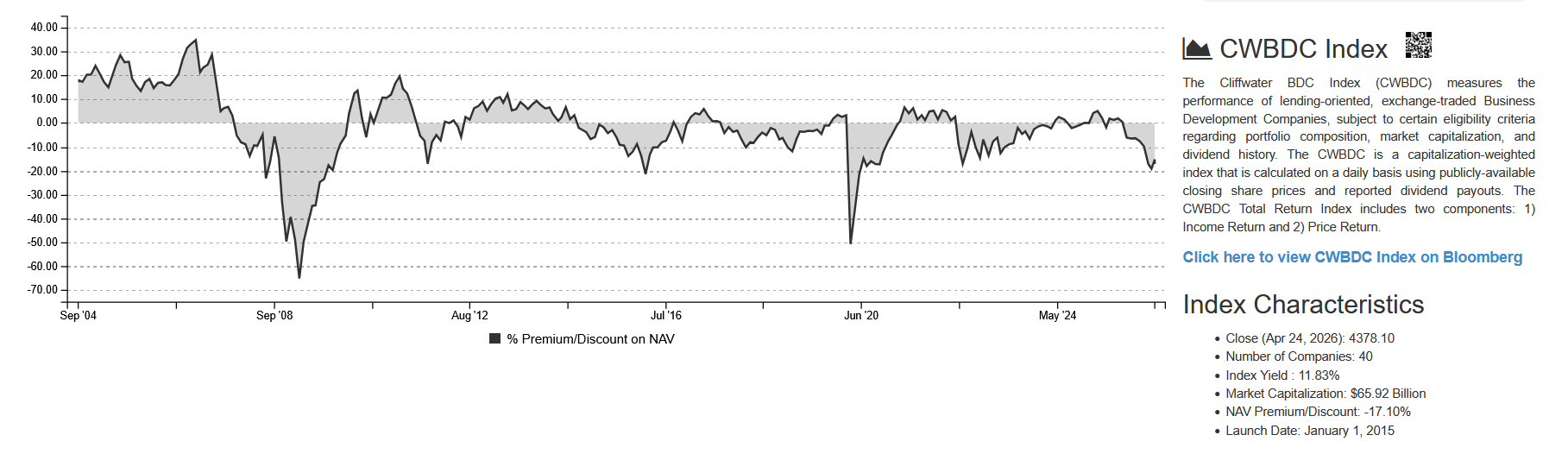

Let us begin by examining the behavior of the market price and pose a direct question: Are we genuinely prepared for this level of volatility?At its core, there are two distinct figures: the Net Asset Value (NAV) and the market price. The difference between the two is referred to as a discount when the market price falls below the NAV, and a premium when it rises above it.Put simply, our task is to identify and seize opportunities — whether they are exceptional or merely compelling. Looking at the chart below, we are currently operating in favorable opportunity territory, with the discount approaching 20%.The truly exceptional buying opportunities of 2008 and 2020 are infrequent. And frankly, only the most courageous investors are able to deploy capital during those periods of extreme panic.This is precisely where income investing reveals one of its greatest strengths: it disciplines us to remain invested and consistently capitalize on such moments.

Source: https://www.bdcs.com/

From a long-term perspective, the total return is good, around 9.5% per year. That is already a useful initial benchmark. But since I am targeting more ambitious returns, I will need to invest only during periods of market stress with high discounts in order to significantly increase those returns and align with my investment logic. Essentially, the challenge is to identify good entry points with discounts between 20% and 30%, and then hold the securities for the very long term.

Source: https://www.bdcs.com/

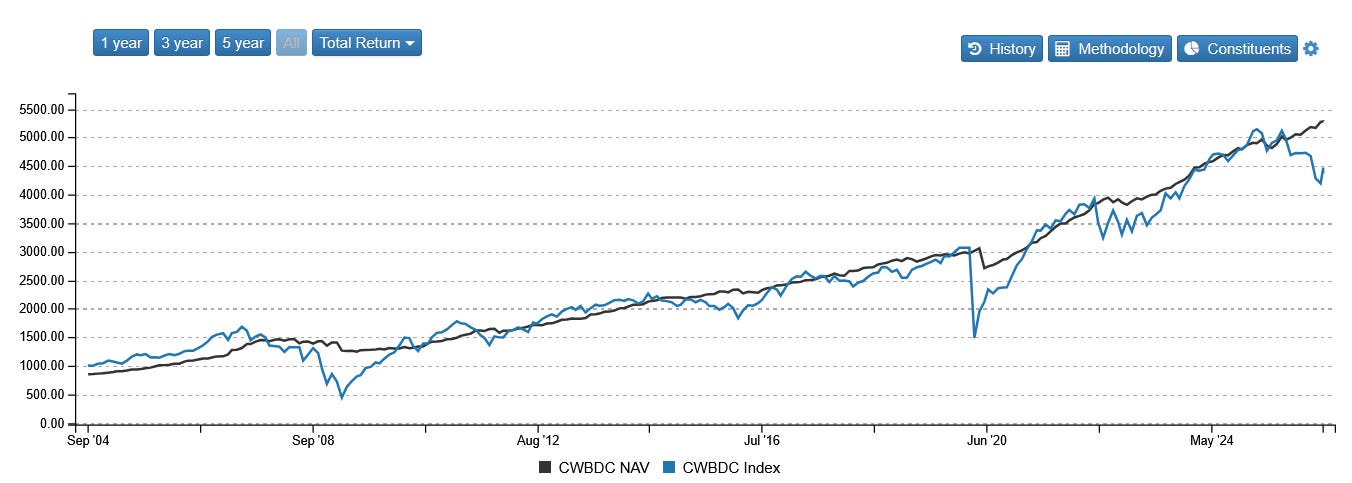

And this is all the more important because, when you look at NAV alone on this type of investment, concern is not a luxury.

Source: https://www.bdcs.com/

At first glance at this chart, many would conclude that BDCs are nothing but yield traps. In reality, this asset class is heterogeneous, so the challenge is to find securities that preserve NAV as much as possible while generating good yields. Because right now, at the end of April 2026, yields are attractive. And there will be other such periods in the years to come. Let’s apply this strategy.

II/ What I buy carefully this month

A/ I build a (modest) long term BDC position right now with BXSL

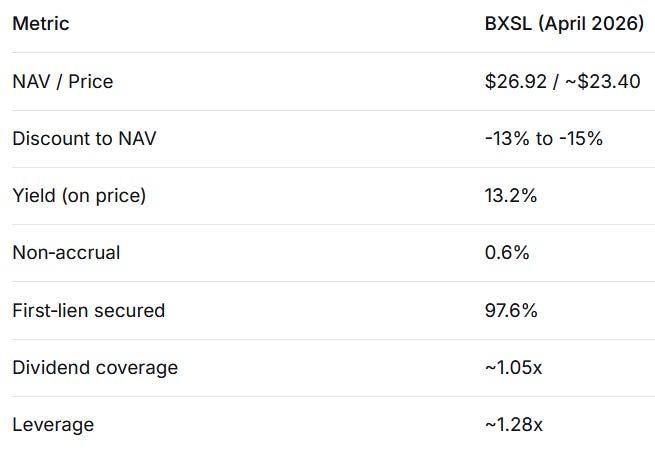

After reviewing many BDCs, I decided to add BXSL (Blackstone Secured Lending Fund) to my global income portfolio. It stands out as a high‑quality name that fits well with my I‑CASH methodology, particularly in the current market environment where several quality BDCs are trading at attractive discounts.

BXSL offers top‑tier portfolio quality (97.6% first‑lien senior secured, 0.6% non‑accrual) backed by Blackstone’s underwriting. The current 13‑15% discount to NAV boosts the yield on market price to 13.2%, while the NAV‑based yield stands at 11.4%. Dividend coverage is comfortable (~1.05x). The NAV decline in 2025 was mainly driven by repayments and modest mark‑to‑market adjustments, not by rising credit losses.

Compared to peers like ARCC (~5% discount), MSDL (~8% discount, higher non‑accrual), or MAIN (premium), BXSL offers a rare combination of quality and a double‑digit discount.

Interest rate sensitivity: a 100 bps cut in SOFR would reduce NII by roughly $0.20‑0.25 per share per year. I am comfortable with this risk as rates are expected to remain elevated in the medium term.

Of course, risks remain: credit cycle, falling rates, and price/NAV volatility. But as a long‑term buy‑and‑hold investor – I never sell – the entry point matters most. In today’s context, BXSL fits perfectly with my discount‑driven income strategy.

Source: https://seekingalpha.com/symbol/BXSL

B/ And another one with MSDL

I also chose MSDL (Morgan Stanley Direct Lending Fund) for my global income portfolio. More discount, less prestige. MSDL offers a highly defensive portfolio (96.2% first‑lien senior secured, 99.6% floating‑rate loans) backed by Morgan Stanley’s underwriting platform. The current deep discount to NAV, one of the widest in the sector, significantly boosts the yield on market price. Non‑accrual remains low at 1.6% of total investments, and the debt‑to‑equity ratio of 1.20x is conservative, providing a stable capital base.

Some risks are high: the dividend was recently reduced from $0.50 to $0.45 per share, and dividend coverage is tight at approximately 1.05x based on recent NII of $0.49 per share. Falling rates would pressure floating‑rate income (99.6% floating), and competition in private credit may compress spreads. But as a long‑term buy‑and‑hold investor (I never sell), the entry point matters above all. At current prices, MSDL offers a deep discount and a double‑digit yield, making it an attractive addition for my discount‑driven income strategy.

Investment Takeaway

As we have seen recently, my portfolio is still too heavily loaded in USD. But that is one of the flaws of my strategy during the deployment phase of my portfolio: I much prefer to invest in a sector that is discounted and, in my opinion, performing well, rather than strictly adhering to diversification criteria. In short, in the I-CASH method, I prioritize H and S over I and C at this stage. I have years ahead to deploy outside the US.

And to answer the initial question, it seems to me that private credit is investable anew. In any case, I am going for it, even though I read many articles in Europe and the US predicting the crash of the century. That crash will come for a reason we will only see too late. And the only consequence will be that my income will temporarily decrease. In the meantime, I continue to invest in my portfolio and, this month, in this sector: high yield, high risk. As I like it and, above all, as I handle it very well. Since I embraced this principle, my performance has been better than what I achieved when I wanted a bit of everything: growth, DGI, high yield. Might as well focus on what I like most.

Yield is never free. But sometimes it’s underpriced.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.