The Anti Petrobras: a Global, Growing 6.4% Quarterly Dividend

A boring high yield company

No dominant government influence among the shareholders. A diversified portfolio of energy sources. A truly international presence. Let’s be clear: Total Energies has nothing in common with Petrobras. Beyond a similarly low P/E ratio, the two companies are a world apart. While one is subject to the volatile winds of political influence, the other has built its strategy on resilience—proven by its ability to maintain and grow its dividend even through severe oil price downturns and the COVID-19 crisis. Total Energies offers income investors a unique proposition: the high yield of an energy major without the traditional excessive risk. It is a bet on a global, pragmatic, and shareholder-focused management team that prioritizes a covered, growing dividend above all else. This is not just an energy play; it’s a quality income play in a sector often short on reliability.

I. A Premier Global Energy Income Play

A/ A Diversified Energy Mix Positioned for Transition

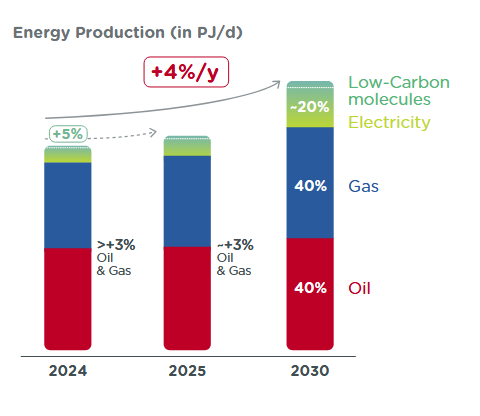

TotalEnergies bridges the worlds of traditional hydrocarbon leadership and emerging low-carbon innovation. With operations spanning over 130 countries, the company is one of the rare global players capable of delivering multiple forms of energy—oil, gas, LNG, renewables, and flexible power—while pursuing consistent growth and disciplined capital allocation.The foundation of TotalEnergies’ strategy rests on two complementary pillars: its robust upstream Oil & Gas business (with a special focus on LNG) and an aggressively expanding Integrated Power segment. The group is targeting a compound annual growth rate in overall energy production of about 4% through 2030, with 95% of future volumes already running or in development. In the coming years, growth will be driven by high-margin oil projects in regions such as the US, Brazil, Iraq, and Uganda, alongside major new LNG starts from Qatar and Malaysia.

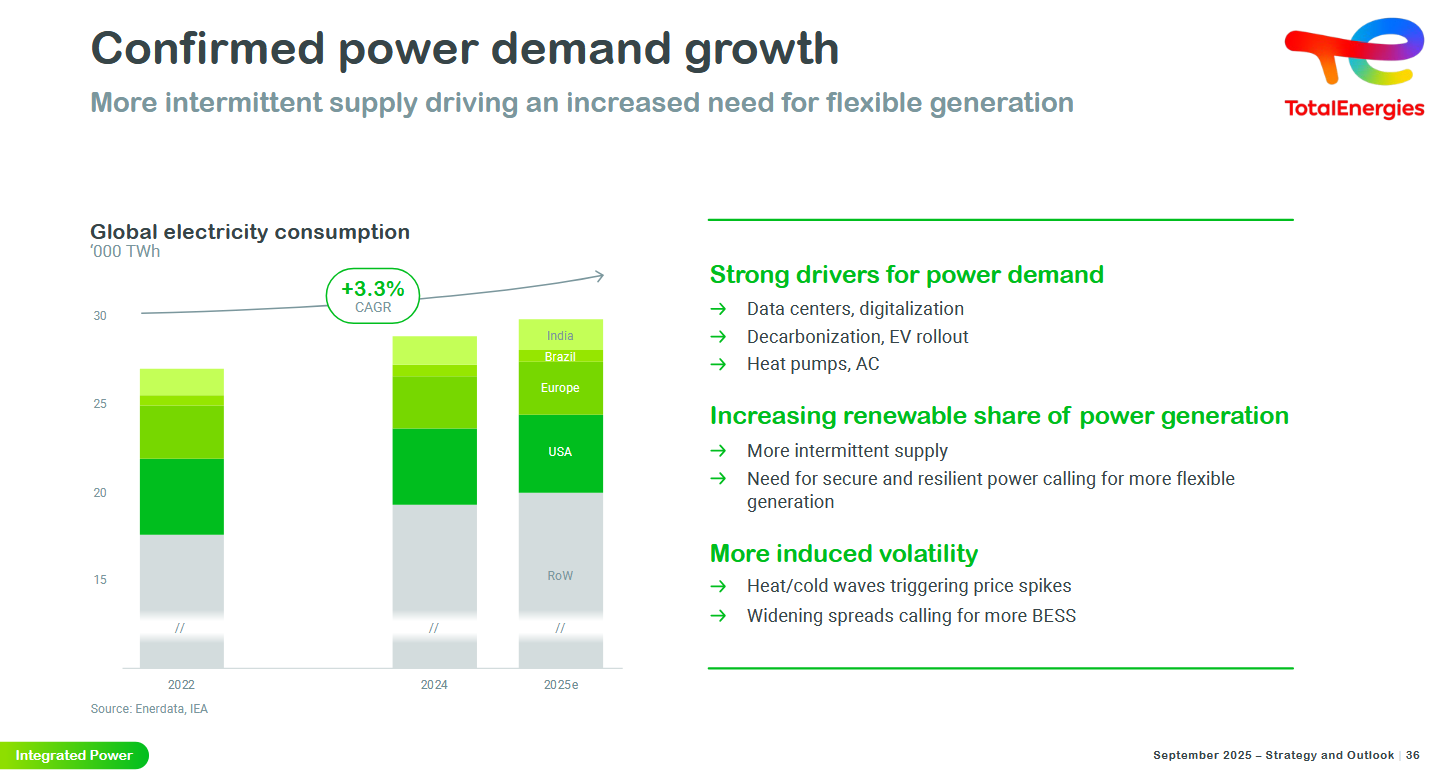

Simultaneously, TotalEnergies is reshaping its power generation mix. Electricity output is set to rise by approximately 20% annually, targeting 100 to 120 TWh per year by 2030—where the majority will be renewable-based, with flexible gas providing the necessary grid stability. The company concentrates investment in major deregulated markets (United States, Europe, Brazil), where its integrated model gives both resilience and pricing power. A rigorous $7.5 billion savings program (Capex and Opex over 2026-2030) underpins its efficiency drive, keeping net Capex for low-carbon investments at $4 billion a year, including a large allocation for Integrated Power.These moves illustrate TotalEnergies’ commitment to delivering “more energy, less emissions.” The company aims to cut Oil & Gas carbon emissions (Scope 1+2) by 40% net from 2015 levels and methane emissions by 80% versus 2020, while also developing carbon capture and storage projects across Europe and beyond.

Source: Total Energies Annual Report 2024

B/ A Reliable Income Investment with Growth Discipline

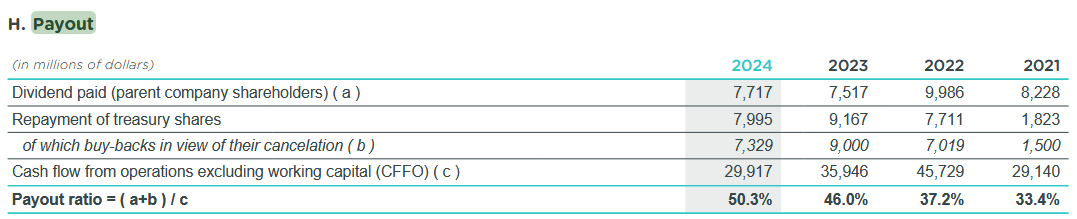

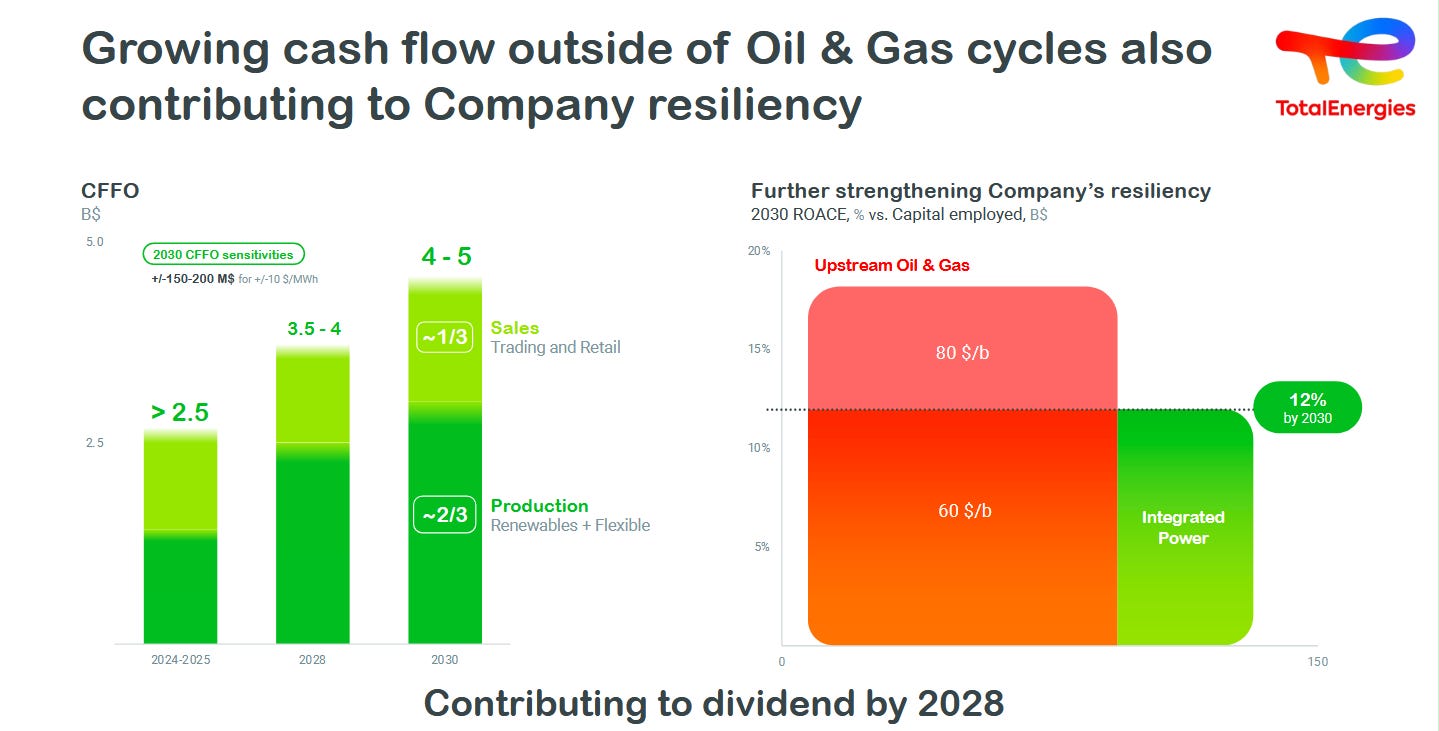

For income-focused investors, TotalEnergies is distinguished by scale, diversification, and a shareholder-centric cash flow philosophy. Unlike peers whose payouts fluctuate with commodity cycles, TotalEnergies has built its reputation on sustaining robust, covered dividends—supported by a resilient, diversified energy mix and strict capital discipline. Since transitioning to a quarterly dividend format, the company’s payout frequency now aligns with US investor standards. The dividend yield, consistently among the highest in the sector (around 6.5% forward as of 2025), is fuelled by strong free cash flow from both Oil & Gas and rapidly expanding power divisions.

TotalEnergies maintains its commitment to shareholder returns, aiming for a payout ratio above 40% of cash flow—complemented by share buybacks that are dynamically adjusted in response to market conditions and earnings growth. The Board recently confirmed a 7.6% increase for the 2025 interim dividend (€0.85/share), underscoring its cycle-resilient growth trajectory.Notably, the firm’s Integrated Power segment is expected to be free cash flow positive by 2028 and achieve a return on average capital employed (ROACE) of 12% by 2030, further enhancing income stability regardless of fossil fuel price cycles.TotalEnergies’ strategic blend of old and new energy, geographic breadth, and financial discipline creates a resilient platform for turning global energy flows into shareholder returns. This approach is rare in the sector—and exemplifies how a leading energy company can embrace the energy transition while ensuring income reliability and capital growth for investors.

Source: Total Energies Annual Report 2024

Despite its robust cash flow engine, TotalEnergies faces sector-wide risks such as energy price cycles, potential windfall taxes in Europe, and the execution risk on long-term energy transition projects. The company’s main listing in Paris also results in structural undervaluation (“French discount”) of up to 15–20% compared to US-listed peers, reflecting historical governance risk, lower liquidity, and home bias among global investors. However, this may offer upside if European sentiment improves, or if the firm’s execution on global diversification is further recognized by international markets.

Beyond its attractive dividend policy and cycle-resilient cash flow, TotalEnergies has delivered strong total returns for long-term shareholders. Over the past decade, the ADR listing in New York has delivered a price total return of 117% (2015–2025), with annualized performance above 8% (including dividends reinvested). While French-listed shares have sometimes traded at a discount to US peers due to lower liquidity and home bias, the company’s recent dual listing and growing global recognition may help close this gap. For income investors seeking a balance between yield, safety, and capital growth, TotalEnergies offers a solid, globally competitive package.

Source: Total Energies Annual Report 2024

II. The Cash Engine: How Hydrocarbons Fund the Dividend & The Transition

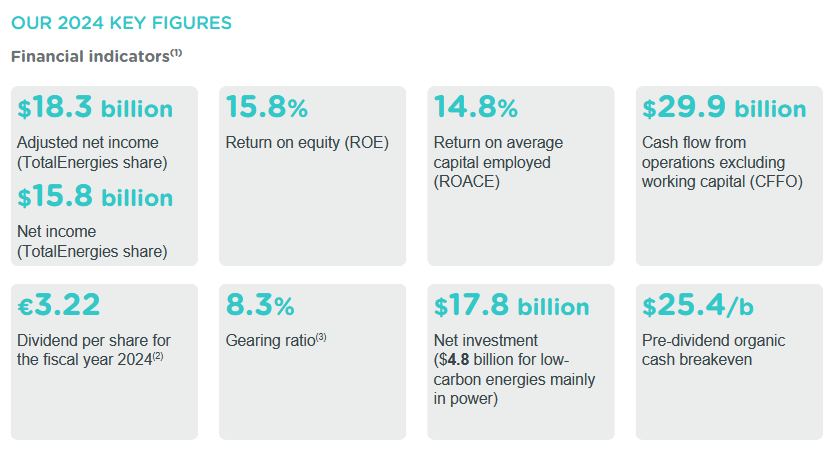

TotalEnergies’ powerful dividend is not sustained by ambitions of going green—it is rooted in robust, recurring cash flows generated by a world-class hydrocarbon portfolio. In 2024, over $30 billion in operating cash flow was delivered, with the overwhelming majority sourced from oil and gas. This provides the surplus that grows the quarterly dividend and finances the company’s entire transition to cleaner energy sources.

A/ Oil: The High-Margin Core

Source: Total Energies Annual Report 2024

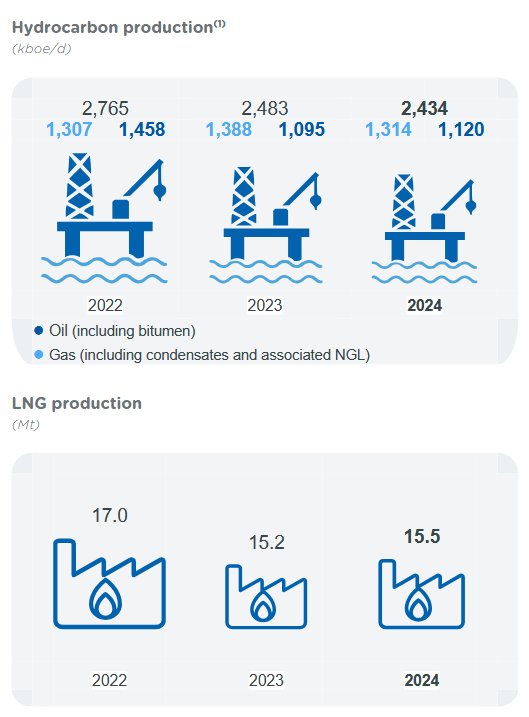

Total Energies remains a top-tier global oil producer, operating major projects across the United States (including deepwater Gulf of Mexico), Brazil, Iraq, and Uganda. These regions are selected not just for volume but for margin stability—the company boasts break-even prices in the $25–30 per barrel range. This means TotalEnergies can deliver healthy free cash flow even when oil markets turn volatile, supporting uninterrupted dividend payments during commodity downturns and macro crises such as COVID-19.The strategy targets a deep, diversified upstream portfolio, balancing long-reserve assets (MENA, Africa) with dynamic, high-return wells in the Americas. Total Energies’ production costs consistently rank among the lowest in its peer group, underpinned by operational discipline and focused capital allocation. The dividend, paid quarterly and currently yielding around 6.4%, is built first on this dependable oil cash engine—not on hopes or political windfalls.

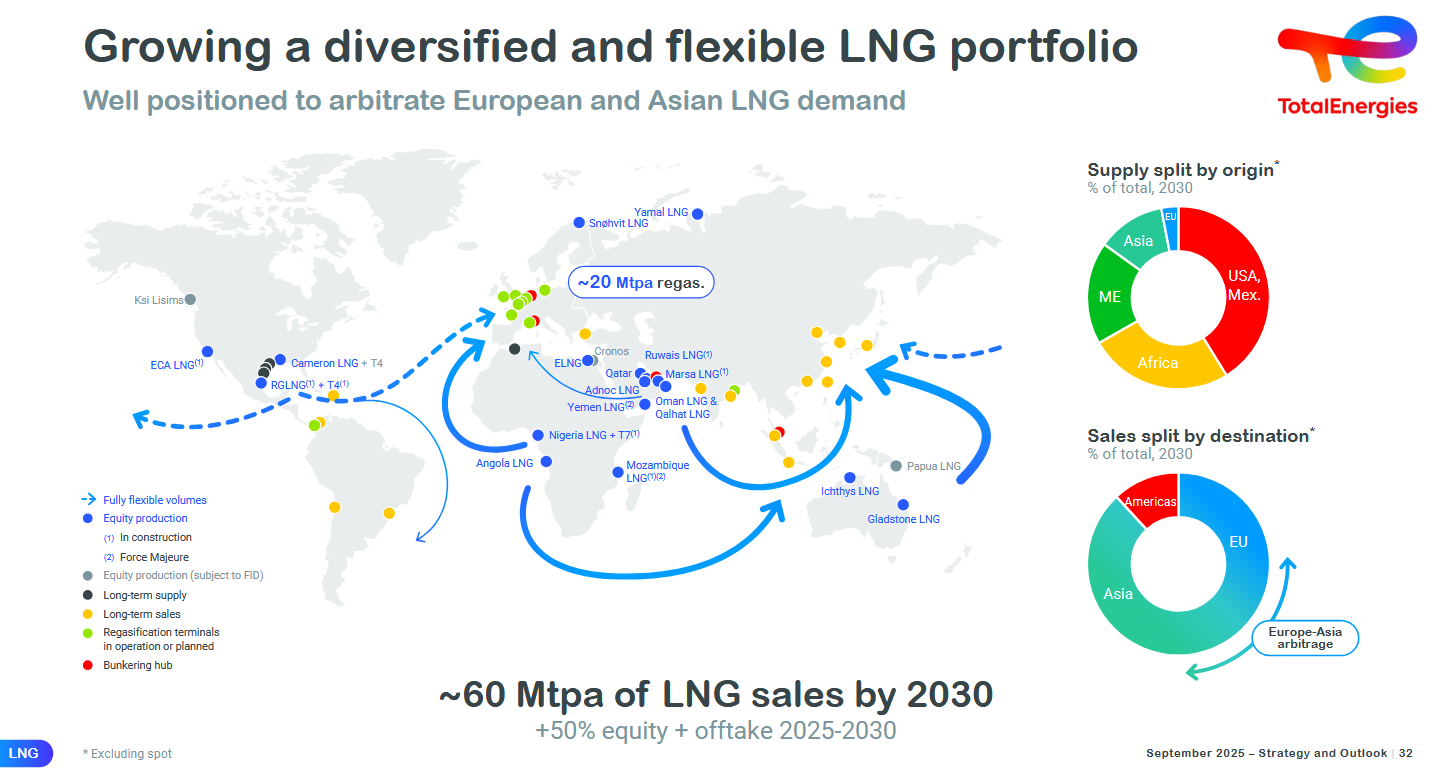

B/ Gas & LNG: The Balancing Force

Gas—especially LNG—is TotalEnergies’ “insurance policy” for shareholders, smoothing profits as oil prices fluctuate. As one of the world’s leading LNG players, Total Energies enjoys a contracted, global business with clients in Asia, Europe, and the Americas. This segment generates steady and predictable income, largely insulated from spot oil volatility.

The company continues investing heavily to grow its LNG portfolio, opening new production in Malaysia and Qatar, and securing access to cost-competitive US supply. Flexible sales contracts—indexed to both Brent and Henry Hub prices—further optimize earnings through dynamic market conditions. LNG acts as a stabilizer, ensuring that the company’s dividend and investment capacity are protected, regardless of swings in global energy pricing.

Source: Total Energies Annual Report 2024

C/ Hydrocarbons: Fueling the Dividend, Securing the Transition

At the core, TotalEnergies’ hydrocarbons fund not only today’s dividend, but tomorrow’s business evolution. Oil and gas supply the free cash flow that enables generous payouts, substantial buybacks, and a substantial annual investment into renewables and integrated power. The current ~6.4% yield remains covered well by core operations, not debt or equity dilution. Even as capex pivots toward decarbonization, the discipline is clear: only surplus cash from hydrocarbons is reallocated—project returns for renewables must match double-digit benchmarks to secure reinvestment.

This self-funding model is what makes TotalEnergies structurally different from state-influenced rivals and sets its dividend appeal apart for income investors. It’s not an aspirational “green story,” it’s a global cash engine transitioning with the times—without sacrificing returns or reliability.

III. Renewables: Funded, Not Forced – And Just as Value-Accretive?

Where many oil majors spend billions chasing green credibility, TotalEnergies does something simpler—and smarter. It funds its transition through profits, not dilution. Roughly 25–30% of annual capex now flows into low-carbon power, solar, wind, and storage. By 2030, management targets 100 GW of gross renewable capacity, positioning the company as a genuine energy producer—not just a fossil firm adding token wind farms.

But for income investors, the burning question is: can renewables match the profitability of fossil fuels, or is this just costly virtue-signaling? The short answer: yes, they’re designed to be value-accretive, though not quite at fossil levels—yet. Total Energies’ upstream oil and gas operations routinely deliver ROACE in the 15-20% range, thanks to low breakevens and scale. Renewables, by contrast, target a solid 12% ROACE by 2030, with Integrated Power turning free cash flow positive as early as 2028. This isn’t chasing headlines; it’s disciplined investing in assets that compound shareholder value without eroding the core cash engine.

Source: Total Energies Annual Report 2024

Take the portfolio: in the US, TotalEnergies is scaling solar farms in Texas and wind projects in the Midwest, leveraging tax credits and long-term PPAs for stable, inflation-linked cash flows. In Europe, offshore wind developments (like the recent French auction win) and battery storage add grid flexibility, capturing premiums in deregulated markets. Brazil’s hydropower and solar hybrids round out the mix, blending renewables with gas for reliability. These aren’t speculative bets—each project must hurdle a 12% IRR threshold before greenlighting, ensuring they stack up against hydrocarbon alternatives on a risk-adjusted basis. Critics might argue renewables face headwinds: higher upfront capex, weather variability, and policy risks. But Total Energies mitigates this through its integrated model—pairing solar/wind with gas peakers for 24/7 dispatchability—and by sticking to mature markets where subsidies are phasing out but demand is surging. The result? Projected electricity sales growth to 100-120 TWh by 2030, with margins rivaling upstream in a post-subsidy world. Funded entirely by hydrocarbon surplus (no new equity issuances), this pivot de-risks the portfolio: as oil/gas provide the ballast, renewables diversify earnings away from carbon pricing and volatility. This pragmatic, balanced approach—fossil cash feeding a renewable transition—explains why Total’s dividend looks not only generous, but structurally secure. It’s proof that green can be gold, without compromising the bottom line.

Source: Total Energies Annual Report 2024

Investment Takeaway

TotalEnergies is not an oil company pretending to be green. It is a world-class cash flow engine using its existing strength to build a durable, multi-energy future.

For any investor building a Global Income Portfolio, TotalEnergies delivers the essential trifecta:

A high ~6.4% starting yield.

A commitment to growing quarterly payments.

A self-funding, resilient business model that de-risks the energy transition.

In a sector defined by volatility, it offers a rare combination of yield, growth, and stability.

For my portfolio, it’s a solid dividend stock, though far from offering a double-digit dividend yield. That said, the strategy here is patience - I’m waiting for a better entry point. I would consider buying when the dividend yield reaches 8%. Given TotalEnergies’ consistent ~7% dividend growth, the yield on cost would quickly approach 10%.

While the current yield doesn’t match Petrobras’s compelling offer, TotalEnergies is a middle risk / middle yield and earns a spot on my watchlist. For now, I’ll be patient and wait for a more attractive valuation. But a mix of Petrobras and Total Energies is perfect for me : a combined 10% dividend yield.

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

Disclaimer: This article is for informational and educational purposes only and should not be considered financial or investment advice. The views expressed are solely those of the author and do not constitute a recommendation to buy, sell, or hold any security. Always conduct your own research and consult with a professional before making any investment decisions.

Thanks, Robots and Chips, for the kind words! I love the Petrobras-TotalEnergies pairing—it's so perfectly contrarian that it just has to work. We'll need to stay patient. I'm working on a Petrobras update for the next few weeks. The coming decade is going to be fascinating for income investing.