The Case for a Chinese Services Small Cap with a Rare 10% Dividend Yield

Betting on the Chinese High Education Market?

In my relentless search for yield across sectors and currencies, I often venture into high-risk, high-reward territories that many income investors avoid. China, despite its well-documented challenges of transparency and volatility, remains an impossible market to ignore for those seeking asymmetric opportunities. Today, I'm analyzing a controversial play: a private education company offering a seemingly unsustainable 10% dividend yield amid collapsing profits. This isn't a stable income pick—it's a high-conviction speculation on a deep-value turnaround story, where the market's panic may have created a rare opportunity. Let's determine whether this is rational investing or reckless yield-chasing.

I/ Bottom-up approach: an Education firm in full expansion

A/ A 22-year-old small cap in full growth

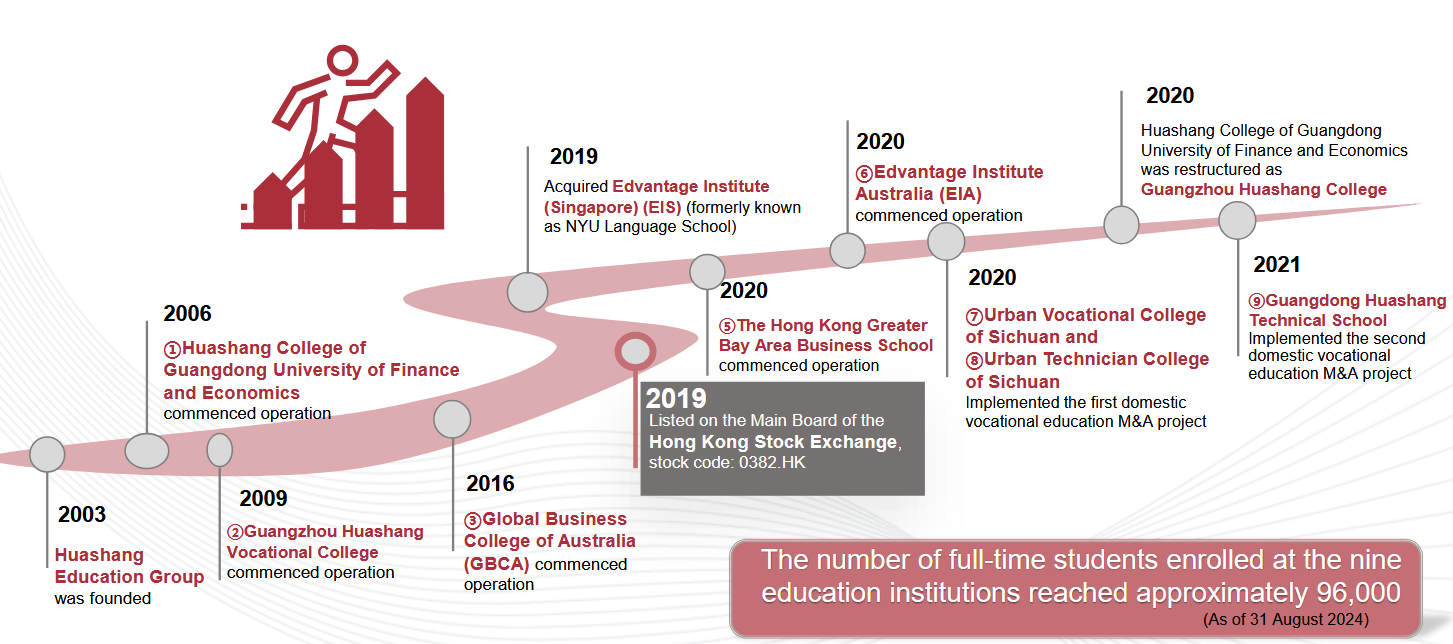

Edvantage Group Holdings (0382.HK) is a leading private higher education and vocational training provider in China’s Greater Bay Area — spanning Guangdong, Hong Kong, and Macau. . Founded in 2003 and publicly listed on the Hong Kong Stock Exchange since 2019, the Group is now moving beyond its home market, accelerating an international strategy that raises both opportunities and execution challenges. As shown below, the company has opened many schools since 2003.

Source: Edvantage Group

With nearly 96,000 students in 2024, Edvantage differentiates itself through a diversified portfolio

Unlock the Full Risk Profile & The Final Verdict

You’ve seen the impressive growth and the crisis-level valuation (4.5x P/E) that delivers a 10% forward dividend yield. But why has the market punished this stock so severely?

The remainder of this deep-dive is hosted on our main platform, where we switch to a Top-Down view to reveal the hidden risks and the high-conviction thesis.

In the full article, you will see:

The IPO History: How a 40% capital loss since 2019 sets the stage for today’s value opportunity.

The Critical Risks: A detailed analysis of the Chinese political risk (Double Reduction Policy) and currency risk that could cut the 10% yield in half.

My Final Investment Takeaway: The three pillars that justify initiating a global income speculation on this turnaround story, collecting 10% for the wait.

To understand the full downside risks and see the logic behind this high-conviction investment, click the button below to read the complete article on our website:

Liked this Deep-Dive? Buy Me a Coffee!

Your support keeps this newsletter independent and research-driven. If this analysis saved you time or gave you a new investment idea, consider making a one-time donation. Every contribution helps me maintain part of the research free and accessible to everyone.

Disclaimer: This article is for informational and educational purposes only and should not be considered financial or investment advice. The views expressed are solely those of the author and do not constitute a recommendation to buy, sell, or hold any security. Always conduct your own research and consult with a professional before making any investment decisions.